Financial technology, commonly known as fintech, has revolutionized the way we handle financial transactions and manage our money. Fintech refers to the innovative use of technology in delivering financial services, making them more accessible, efficient, and user-friendly. As a result, traditional banks are facing increasing competition from fintech companies that are challenging their dominance in the financial industry.

Globally, fintech has experienced remarkable growth over the past decade. According to a report by PwC, global investment in fintech ventures reached $112 billion in 2018 alone. This rapid expansion is not limited to developed economies; emerging markets like Uzbekistan have also witnessed significant advancements in their fintech landscape.

In Uzbekistan specifically, payment companies have emerged as key players within the fintech space. These entities offer alternative methods for conducting transactions outside of traditional banking channels such as cash or physical branches.

Paynet is one oldest and first payment companies in the market. Paynet was one most popular payment methods in Uzbekistan at the initial stages of development. The company enabled payments for mobile services and utilities through its chain kiosks all over the country. However, smartphones and internet penetration made the company move towards mobile application services at later stages of growth.

Another prominent example is Payme – a leading mobile payment platform that facilitates seamless peer-to-peer transfers and online payments through smartphones. Payme has gained widespread popularity among users due to its convenience and ease of use.

Click payments system launched the first USSD payments and peer-to-peer transfer in the market. It has made significant contributions towards transforming Uzbekistan’s payment landscape by offering secure online transactions with minimal friction.

These payment companies pose formidable challenges to traditional banks for several reasons:

-

Accessibility: Fintech firms leverage digital technologies such as mobile applications and internet-based platforms that provide convenient access anytime and anywhere for customers. This accessibility appeals especially to younger generations who prefer using their smartphones rather than visiting brick-and-mortar bank branches.

-

Enhanced User Experience: Fintech companies place great emphasis on user experience by designing intuitive platforms that are easy to navigate, transparent in terms of fees or rates, and personalized according to individual preferences. These customer-centric approaches have been instrumental in attracting tech-savvy individuals who value simplicity and convenience.

-

Innovation: Fintech companies continuously introduce innovative solutions that address pain points within the traditional banking system. They provide services such as digital wallets, online lending platforms, investment apps, and robo-advisors which offer greater flexibility and tailored financial solutions.

-

Financial Inclusion: Payment and fintech entities are instrumental in promoting financial inclusion by reaching underserved populations who may not have access to traditional banking services. With simplified account opening procedures and digital payment solutions, these entities bridge the gap between unbanked individuals and formal financial systems – improving their economic opportunities.

-

Cost-efficiency: Traditional banks often involve higher fees for various financial services compared to fintech companies which can offer lower-cost alternatives due to their streamlined operations and innovative business models.

Payment and fintech entities challenge traditional banks by leveraging technology, providing superior user experiences, offering cost-efficient solutions, promoting financial inclusion, fostering innovation at a faster pace, and presenting opportunities for collaboration. As the fintech industry continues to grow globally and within Uzbekistan specifically, traditional banks must adapt their strategies to remain competitive in the rapidly changing financial landscape.

In the next sections, we will delve deeper into the growth numbers and statistics surrounding fintech in Uzbekistan, explore the factors driving this growth, examine challenges faced by these emerging players, and highlight potential collaboration opportunities between banks and fintech firms.

Payment ecosystem

The fintech ecosystem in Uzbekistan is still relatively nascent compared to other countries. However, the government has recognized the potential of fintech and has taken steps to promote its growth.

The country has witnessed a rise in digital payment solutions. Payment companies like Payme, Click, Paynet and others are gaining popularity for their ease of use and convenience. These platforms allow users to make payments, transfer money, and pay different bills.

Payment companies received popularity because, unlike the banks in the market, they were the first to introduce user-friendly applications and methods to make peer-to-peer transfers and payments to different services. For example, Click was one of the first companies to introduce p2p transfer over USSD. This service received popularity among customers, especially in the regions of the country where there were almost no internet connection. Even though the internet penetration in the country has significantly improved since then this was the feature that made the Click one of the leading fintech companies in the market.

Payme is another company that led the mobile payments revolution in Uzbekistan by introducing one of the first mobile payment applications. Initially started as p2p transfers and simple payments application the company now offers a wide range of financial and payment services.

If non-cash P2P transfers gave birth to the growth of fintech in the market now companies moved beyond simple transfers and moving towards building an ecosystem of products or super apps. This is largely because the current tariff landscape leaves payment service providers (PSPs) with sufficient funds for the rapid development of digital services. As a result, about 60 PSPs are operating in the country, which has fundamentally transformed the methods of transferring C2C and partially C2B funds.

Even though P2P transfers remained a core feature on almost all the payment applications companies did not stop on this feature only. Currently, leading payment applications offer their customers payments of different utility services, bill payments, integrations with international payment services, loan payments and the ability to buy non-financial services such as insurance and others.

When we discuss the fintech industry of the market we must mention three important services that payments companies introduced to the market that played a significant role in the adoption of non-cash payments.

Click and Payme were the first two payment companies that introduced in-store QR payments and remain leaders in this market segment. The introduction of QR payments was important not only for end users but for merchants too. With the growth of smartphone usage especially among the younger generation QR payments create a significant push towards a cashless economy.

Another important service that was introduced to the market by payment companies was mobile wallets. This service allows customers to create their mobile wallets with payment companies and the main advantage of this service is that it doesn’t require customers to have bank cards or accounts. That way this service promotes financial inclusion and allows any customer to get access to financial and payment services.

Last but not least payments are leaders in e-commerce integrations where you will see almost no banks. Most of the marketplaces and e-commerce websites integrate with Payme and Click as most of the customers (combined 20+ million) use these two payment services.

We must also mention that payment companies offer not only B2C services. Lately, most of the local and some international payment companies started actively offering b2b payment and merchant services and one of the driving forces in this direction was the growth in online sales.

The current fintech ecosystem of Uzbekistan consists of not only payment companies. In the last several years banks also started actively launching their mobile applications and offering payments as well as digital banking services. However, unlike payment companies, banks were late to the market and are significantly behind in UX and offering some of the popular services such as QR payments, digital wallets and non-financial services.

Growth numbers and statistics

The fintech industry in Uzbekistan has witnessed remarkable growth and transformation in recent years. Let’s take a closer look at some key statistics that highlight the progress and impact of this burgeoning sector.

Analysts note a rapid increase in demand for payment services from non-banking services. According to the Central Bank, this is facilitated by favourable conditions for market participants.

As of January 1 2023, there were 47 licensed payment organizations in Uzbekistan, according to the Central Bank.

Users:

-

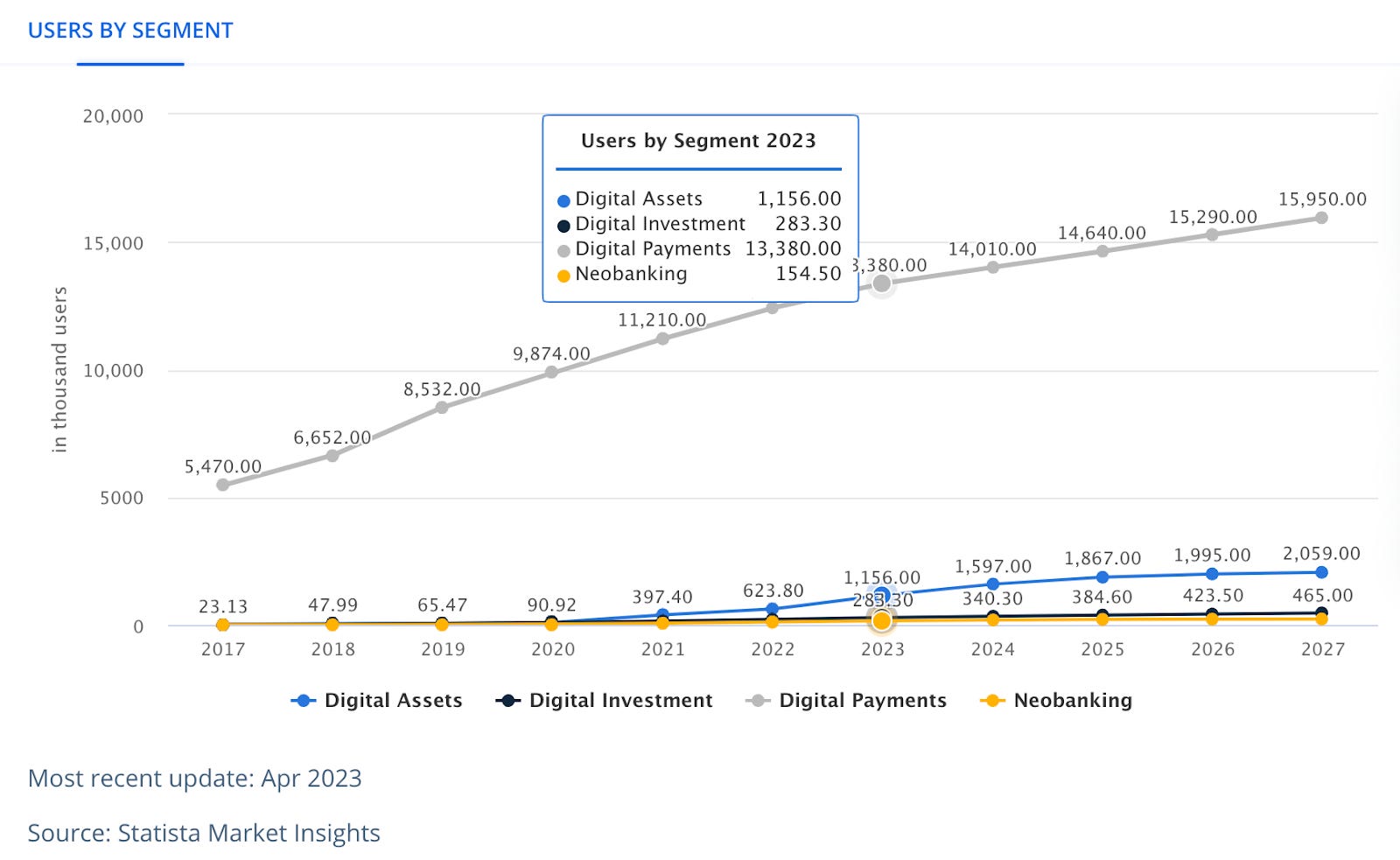

According to Statista, the number of users of digital payment services grew from 5,4 million users in 2017 to over 12 million in 2023

Transaction volume by payment organizations in 2022:

-

In 2022, payment organizations carried out transactions worth 116 trillion. sum, which is 2.1 times more than in 2021.

-

The volume of transactions in payment services continues to grow every quarter. If in January-March it amounted to 21.6 trillion soums, then in October-December – 38.2 trillion, or 76.8% more.

-

The most popular purpose of transactions in payment services was payment for mobile communications – over the year it reached 10.46 trillion soums, 3.17 times higher than the previous year. The largest increase was shown by utilities – 3.4 times or 8.94 trillion soums.

-

The volume of online payments for government services also increased noticeably, amounting to 6.1 trillion soums or 236% more than the figures for 2021. Loan payments during the same time increased 2.6 times – to 3.64 trillion soums.

-

The number of QR codes installed in businesses by the information system increased by only 8 thousand and amounted to 99 thousand units. Despite this, the volume of transactions made through this system increased from 14.9 billion soums in 2021 to 191.6 billion soums in 2022, and the number increased 4.2 times and reached 63.2 thousand units.

-

In 2022, the volume of transactions using NFC technology increased 2.1 times compared to 2021 and reached 25.5 trillion. Sum

-

In-store payments (661 billion soums) and payments for transport services (767 billion soums) more than doubled. On the other hand, payments for Internet services through payment services decreased by almost a third – to 866 billion soums.

-

Over the past year, 11.6 million transactions (+79.2%) worth 273.25 billion soums (+60%) were carried out through electronic money systems (e-wallets). A particularly strong increase was observed in the last quarter when the volume of payments amounted to 124.17 billion soums – almost twice as much as the previous quarter.

Transaction value by payment organizations in 2022:

-

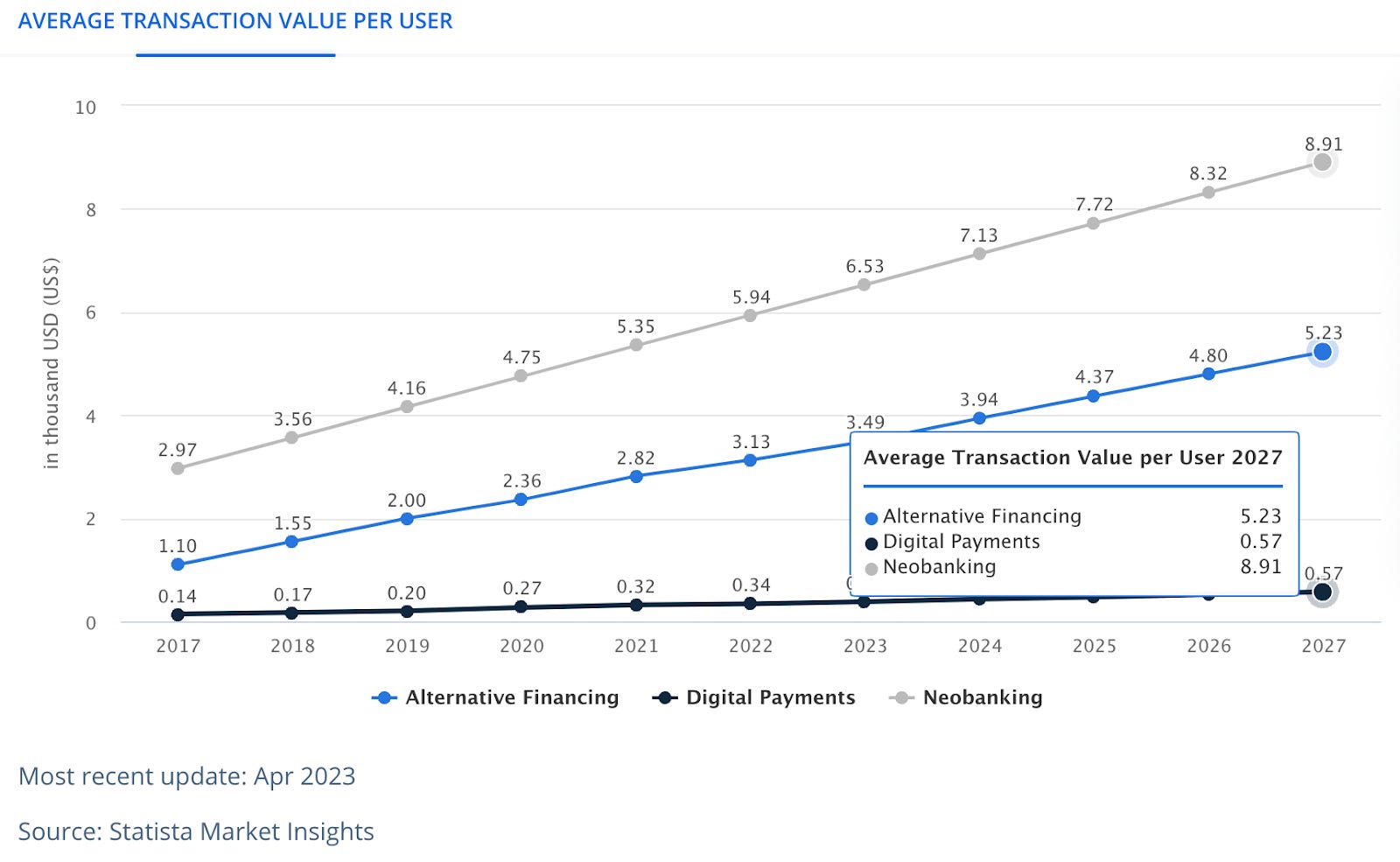

The average transaction value per user over digital payment services was 0.34 USD in 2022 and is expected to grow to 0.57 USD by 2027

Growth factors

Fintech, or financial technology, is a rapidly growing sector in Uzbekistan, with several factors contributing to its rise.

Digitisation of the economy and government services:

The digitisation of the economy and government services of Uzbekistan is a strategic move by the government and one of the main factors behind the growth of fintech in the country. The government has implemented various programs and strategies to foster the development of information and communication technologies (ICT) and to build a ground for consumers and businesses to get access to various services digitally.

Users of payment companies can make payments to different government services such as education, healthcare, bills for government services etc. directly in the applications. The numbers show that payments for utility services which were digitised as part of the shift toward digitisation and payments for government services were among the top three payment categories in 2022. The volume of online payments for utilities increased 3.4 times or 8.94 trillion soums and government services amounted to 6.1 trillion soums or 236% more than the figures for 2021.

Technology

Technological advancements, such as the rise of smartphones and mobile internet, have made it easier for people to access financial services, regardless of their location or access to traditional banking services. In 2019, the Law “On Payments and Payment Systems” was adopted, which determined the legal status of the main categories of fintech business and established concepts such as electronic money and payment services. This enabled payment companies to launch their e-wallets and if before users had to have a banking card to use payment services now they could create their e-wallets with payment services and start using financial services. On the other hand, at the end of 2020, banks and payment organisations were allowed to carry out identification not only by the physical method but also by digital biometric tools. By the end of 2022, 26 commercial banks and 13 payment organizations had implemented this technology. This, in turn, has significantly expanded the ability of clients to remotely use banking and payment services (opening a bank account, opening an electronic wallet, microloans, receiving funds through international money transfers) without directly visiting bank branches or payment organizations. This is particularly beneficial for unbanked populations and people in remote areas.

QR payments are becoming one popular payment method, especially among the younger generation. At the moment Payme and Click are leading payment companies that offer QR payments and no banks except Uzum Bank which operates almost like a payment company offer QR payments. The advantage of QR payments for merchants is unlike card-based payment systems, QR code payments do not require expensive point-of-sale terminals or high transaction fees. The number of transactions in the QR Online system more than quadrupled – to 63,287. At the same time, the number of payment QR codes increased only by 8 thousand. The volume of payments using QR codes in 2022 amounted to 191.6 billion soums. This is 12.8 times more than the previous year. The development of infrastructure for payments via NFC smartphone devices also continues. Currently, the Tap-to-phone system is used by more than 2,300 enterprises. The volume of NFC transactions over the past year increased 2.1 times and reached 25.5 trillion sums.

E-commerce

E-commerce and marketplaces are two sectors of the digital economy that are fostering the growth of fintech and payments. According to KPMG in 2022, the e-commerce market in Uzbekistan achieved a remarkable milestone, reaching a size of 311 million US dollars. Fintech and payments are the technologies and services that facilitate the transfer of money and value between parties in e-commerce transactions. Fintech and payments are the technologies and services that facilitate the transfer of money and value between parties. Uzum one of the biggest ecosystems in Uzbekistan has its marketplace, food delivery, banking, etc. and after the merger with Click one of the biggest payment companies has its payment services. Uzum enables its customers to make payments for purchases directly in the banking at delivery points and this creates a unique experience. Due to their scale and huge customer base, Payme and Click have become two must-have payment services on almost all e-commerce stores and marketplaces. BNPL is another instrument that is popularised through e-commerce sales pushing the boundaries of cashless payment through payment and BNPL apps. E-commerce is driving innovation in merchant payment services too for example with the help of BNPL merchants can attract more customers and increase sales. Merchants focusing on integrations with international payment gateways to sell internationally.

Consumers

Consumers are increasingly demanding convenient, fast, and user-friendly financial services. Fintech solutions often offer a more streamlined and customer-centric experience than traditional banking systems. To meet customer needs and wants fintech moving towards building super apps where financial, non-financial and e-commerce services are combined in place. Click and Payme are the two biggest super apps in the market, however, other players are following trends for example Humans a virtual network operator also working actively in that direction.

Challenges

Fintech companies are revolutionizing the financial sector by offering innovative solutions for payments, lending, investing, and more. However, operating in a highly regulated industry poses many challenges for these companies.

One of the most significant challenges is compliance requirements, which vary across different regulatory organisations in Uzbekistan. Compliance requirements can affect various aspects of fintech operations, such as data security, customer verification, anti-money laundering, tax reporting, and consumer protection. Fintech companies need to ensure that they comply with all the relevant laws and regulations in the markets they operate in, or they may face legal consequences, reputational damage, or loss of customers.

– Anti-money laundering and counter-terrorism financing (AML/CTF): Fintech companies are exposed to the risk of being used for money laundering or terrorism financing activities, especially if they offer services such as remittances, payments, lending or crowdfunding. Therefore, fintech companies need to comply with AML/CTF regulations in the markets where they operate, which may include conducting customer due diligence, monitoring transactions, reporting suspicious activities or freezing assets. However, AML/CTF regulations are not always consistent or aligned with international standards, and pose challenges for small fintech companies in terms of implementation, cost and scalability.

– Taxation: Fintech companies may face taxation issues in emerging markets, such as double taxation, withholding tax or value-added tax. These issues may arise due to the cross-border nature of fintech services, the lack of clarity on the tax residency or permanent establishment of fintech companies or the absence of tax treaties or agreements between countries. Taxation issues may affect the profitability and competitiveness of fintech companies in emerging markets.

To overcome this challenge, regulators need to invest in compliance expertise, technology, and partnerships that can help them navigate the complex regulatory landscape and adapt to changing customer expectations.

Conclusion

In conclusion, the fintech ecosystem in Uzbekistan is experiencing remarkable growth and presents promising opportunities for both local and international players. The statistics and numbers demonstrate the upward trajectory of this sector, indicating a strong demand for innovative financial solutions among consumers.

The factors driving fintech growth in Uzbekistan are diverse. Firstly, the government’s commitment to digital transformation and economic reforms has created an enabling environment for fintech companies to thrive. Additionally, a young tech-savvy population with increasing access to mobile devices and internet connectivity further fuels the adoption of fintech services.

However, it is important to acknowledge the challenges faced by fintech companies operating in Uzbekistan. Regulatory frameworks are still evolving, requiring more clarity and flexibility to accommodate innovative business models while ensuring consumer protection.

Despite these challenges, there is optimism within the industry as stakeholders collaborate towards addressing these issues collectively. The government’s efforts towards regulatory advancements coupled with initiatives fostering collaboration between traditional financial institutions and fintech firms indicate positive developments on the horizon.

As we look ahead, it is evident that continued investments in technology infrastructure, talent development programs, and supportive policies will be crucial elements in shaping a thriving fintech landscape within Uzbekistan.

Overall, it’s an exciting time for fintech in Uzbekistan as innovation continues to reshape the financial services industry. With a sustained focus on overcoming challenges collaboratively while capitalizing on growth drivers present within the country’s dynamic market conditions, we can expect further evolution of this flourishing sector.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.finextra.com/blogposting/25070/deep-dive-payments-in-uzbekistan?utm_medium=rssfinextra&utm_source=finextrablogs