As emerging technologies converge, the world is steered towards new digital money and payment forms. With over 100 countries exploring the potential of central bank digital currency (CBDC), several central banks have already begun pilot projects or even issued their CBDCs.

Despite the general agreement that CBDC should coexist with existing forms of money and complement them, the pace of adoption has been sluggish.

This slow adoption can be attributed to the implications and prerequisites of digitising central bank money. However, central banks must achieve key policy objectives such as financial inclusion and replacing declining cash usage.

To ensure successful CBDC implementation, learning from past payment innovations and investigating incentives that can drive adoption is essential.

This article focuses on a working paper by the International Monetary Fund (IMF) titled which outlines four crucial lessons that can guide the development and implementation of CBDCs.

These lessons cover the essential attributes that CBDC should possess, the channels through which CBDC adoption can be facilitated, the role of central banks in incentivising CBDC service providers, and the establishment of data-sharing arrangements.

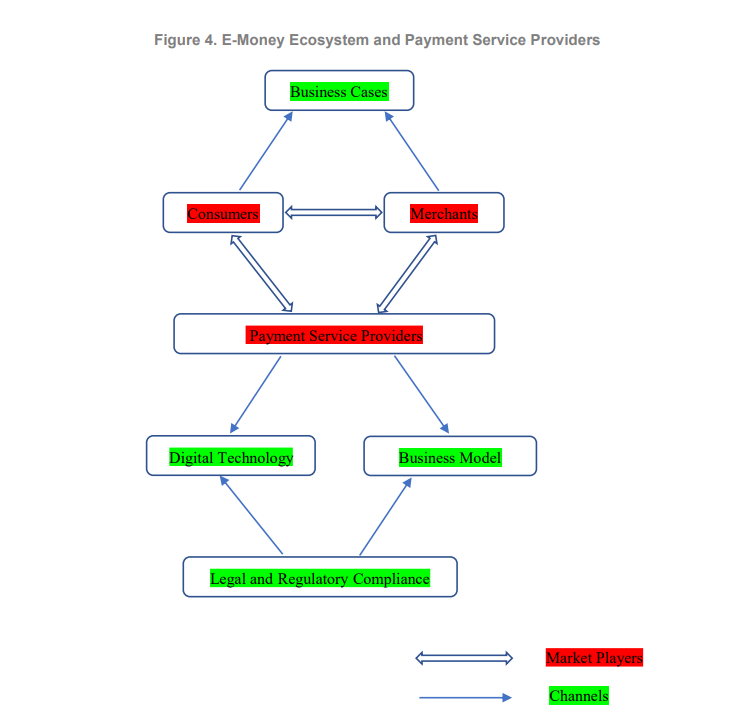

The role of payment service providers

So far, little research has been conducted on the functional role of payment service providers (PSPs) in CBDC adoption. Most CBDC experiments have adopted a two-tier architecture incorporating “hybrid” and “intermediated” models.

Central banks have designed fee structures and pricing models, yet there’s scant analysis of the incentive structures and business models of second-tier PSPs like banks and non-banks.

Unless these PSPs can establish sustainable business models for CBDC provision, the adoption of CBDC will be too limited to allow central banks to achieve their policy objectives.

This analysis draws lessons from six Asian e-money schemes operated by technological companies or platforms (often called “Big Techs”), including Alipay, WeChat Pay, Paytm, GoPay, GrabPay, and ShopeePay.

These schemes have successfully promoted e-money adoption by responding to unmet user demand for payment services, thanks to their skilful exploitation of economies of scale and scope.

The key attributes and adoption channels of these e-money schemes could be instrumental for CBDC adoption. Additionally, countries can harness CBDC to promote contestability in payment systems.

CBDC should embody four key attributes: trust, convenience, efficiency, and security, and its adoption can be facilitated through leveraging digital technology, targeting use cases, developing sustainable business models, and complying with legal and regulatory requirements.

Rapid growth in Asia

The proliferation of e-money schemes in Asia can be attributed to various factors that have created a favourable environment for their rapid growth.

This region boasts a youthful population, high urban population density, low financial inclusion and bank penetration rates, a burgeoning middle class, and swift technology adoption. Together, these elements have empowered e-money schemes to overcome conventional payment barriers.

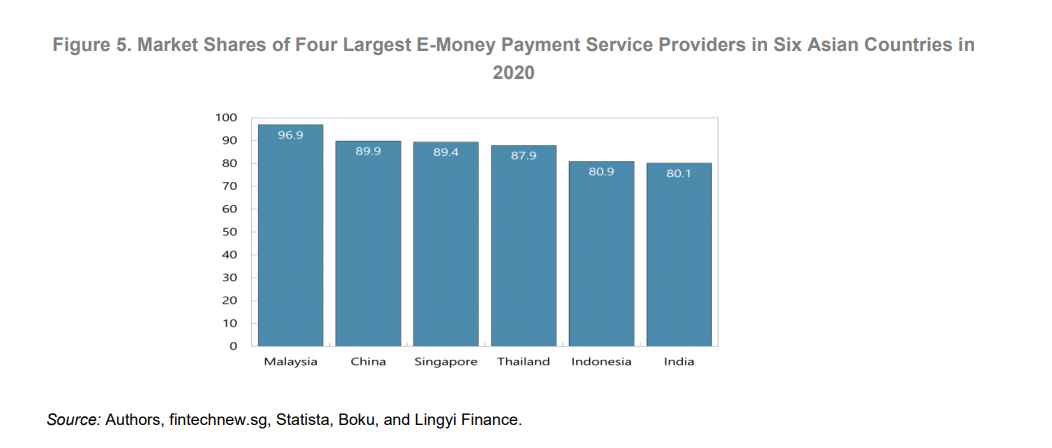

Despite a high level of market concentration, the competition in this industry is fierce, as exemplified by the rivalry between Alipay and WeChat Pay in China.

During the early 2000s, payment services in Asia lacked vital attributes such as convenience, efficiency, and trust. As various use cases like e-commerce, social networks, transportation, food delivery, and online media rapidly increased in popularity, the existing payment services failed to meet the growing demand.

Furthermore, the diverse buying patterns in many Asian countries necessitated more efficient and customised payment solutions.

Asian banking-based payment systems in the early 2000s fell short of providing convenient, efficient, secure, and cost-effective payment services. For example, China’s payment systems were hindered by an outdated payment-processing environment and the absence of a mature credit card market.

In Indonesia, a significant portion of the population remained unbanked, leading to limited e-commerce growth. Additionally, low merchant acceptance and limited utilisation of digital banking further hindered the development of the e-commerce sector in the country.

Promoting financial innovation to build trust and confidence

In the process of e-money adoption in Asia, there are distinct stages that illustrate the evolution of this digital payment method. The first stage focuses on promoting financial innovation to build trust and confidence among users.

To establish a foundation of trust, all six e-money schemes implemented mechanisms to safeguard customers’ funds and transactions. This included connecting e-wallet payment services to regulated bank escrow accounts and creating compensation schemes to instil confidence.

It is worth noting that Alipay took a pioneering role by implementing a policy of fully reimbursing users for any losses resulting from fraudulent activities.

Similar measures were also introduced by other prominent e-money platforms such as GoPay, GrabPay, ShopeePay, and Paytm. These collective efforts aimed to build trust and reassure users regarding the security of e-money transactions.

Leveraging digital technology

The adoption of e-money in Asia can be divided into two stages. In the first stage, the focus is on promoting financial innovation to build trust and confidence among users.

E-money schemes implement mechanisms to safeguard funds and transactions, such as connecting e-wallets to regulated escrow accounts and offering compensation schemes for fraud losses. This establishes a foundation of trust and reassurance for users.

The second stage involves leveraging digital technology, targeting specific use cases, and developing sustainable business models to enhance convenience and efficiency.

E-money PSPs utilise QR codes as a cost-effective alternative to credit cards, enabling cheaper and faster online and offline transactions. By bundling e-money services with established platforms like e-commerce, ride-hailing, social networks, gaming, and cross-border payments, PSPs create seamless user experiences and expand their networks.

To ensure sustained revenue, e-money PSPs collect fees primarily from merchants rather than consumers. They generate interest revenue from depositing customers’ funds and engage in cross-subsidization by supporting other financial services.

Cost management is crucial, with PSPs utilising digital technology to reduce fixed costs and offering pricing strategies that align with merchants and customers.

Complying with legal and regulatory policy to strengthen security

E-money PSPs in Asia have benefited from government support and have complied with legal and regulatory policies to enhance the security in adopting e-money.

Governments, such as in China, have invested in robust digital infrastructures that underpin e-money payments and implemented policies to promote digital finance. For example, India’s demonetisation policy played a role in attracting new customers to platforms like Paytm.

Through diligent adherence to legal and regulatory framework stipulations, several companies have procured or acquired the requisite licenses. Alipay, for instance, has procured a payment license while augmenting its portfolio with additional licenses pertinent to financial services.

Similarly, GoPay and GrabPay have also obtained the necessary licenses through strategic acquisitions and partnerships. Furthermore, E-Money PSPs have meticulously complied with customer funds, technology, and information security regulations.

Alipay, for instance, transferred customer funds to its reserve account at the People’s Bank of China to mitigate risks. At the same time, GoPay and GrabPay adhered to QR code standards and engaged with regulators to support standardisation. Compliance with regulations ensured the protection of users and fostered trust in e-money systems.

Key insights from the adoption of E-Money in Asia

Asia’s e-money adoption offers valuable insights for CBDCs adoption. PSPs have leveraged digital technology, targeted use cases, and adhered to regulations to promote user convenience, efficiency, and trust. This and strategic data use allowed personalised financial services and competition. However, maintaining privacy and market contestability remains crucial.

These lessons are vital to CBDC implementation. CBDC providers need to apply similar strategies, focusing on scalability, convenience, consumer-merchant connection, cost-covering business models, and compliance with legal requirements, including Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT) and privacy protection.

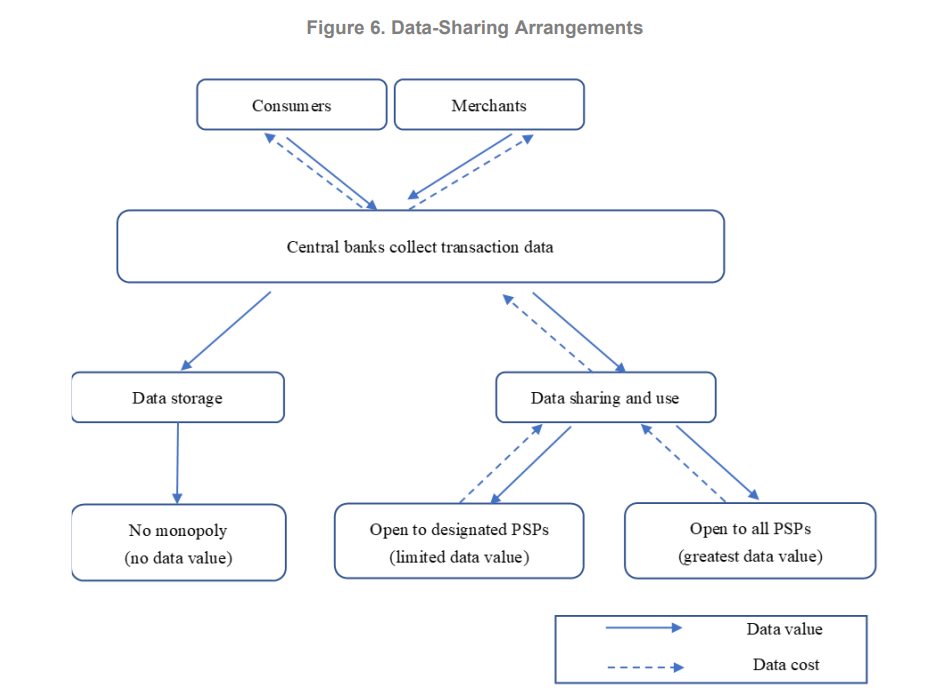

CBDCs can also address data silos seen in e-money PSPs and enhance competition. Data-sharing arrangements based on user consent could integrate CBDCs into existing systems, disrupt data monopolies, and capitalise on data without infringing privacy. Moreover, CBDCs can increase market contestability and place private money under regulatory oversight.

With policy support and clear guidelines, central banks can leverage CBDCs to manage the evolving financial landscape, protect consumers, and regulate competition. These learnings are essential across varying economic structures and payment landscapes for effective CBDC adoption.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://fintechnews.sg/76019/crypto/imf-shows-how-central-banks-can-learn-from-e-money-for-cbdc-success/