- US ISM Services Index unexpectedly surges to a six-month high, boosted on robust new orders and strong hiring

- ECB’s Kazimir prefers a September rate to later and Knot thinks markets underestimating September rate hike chance

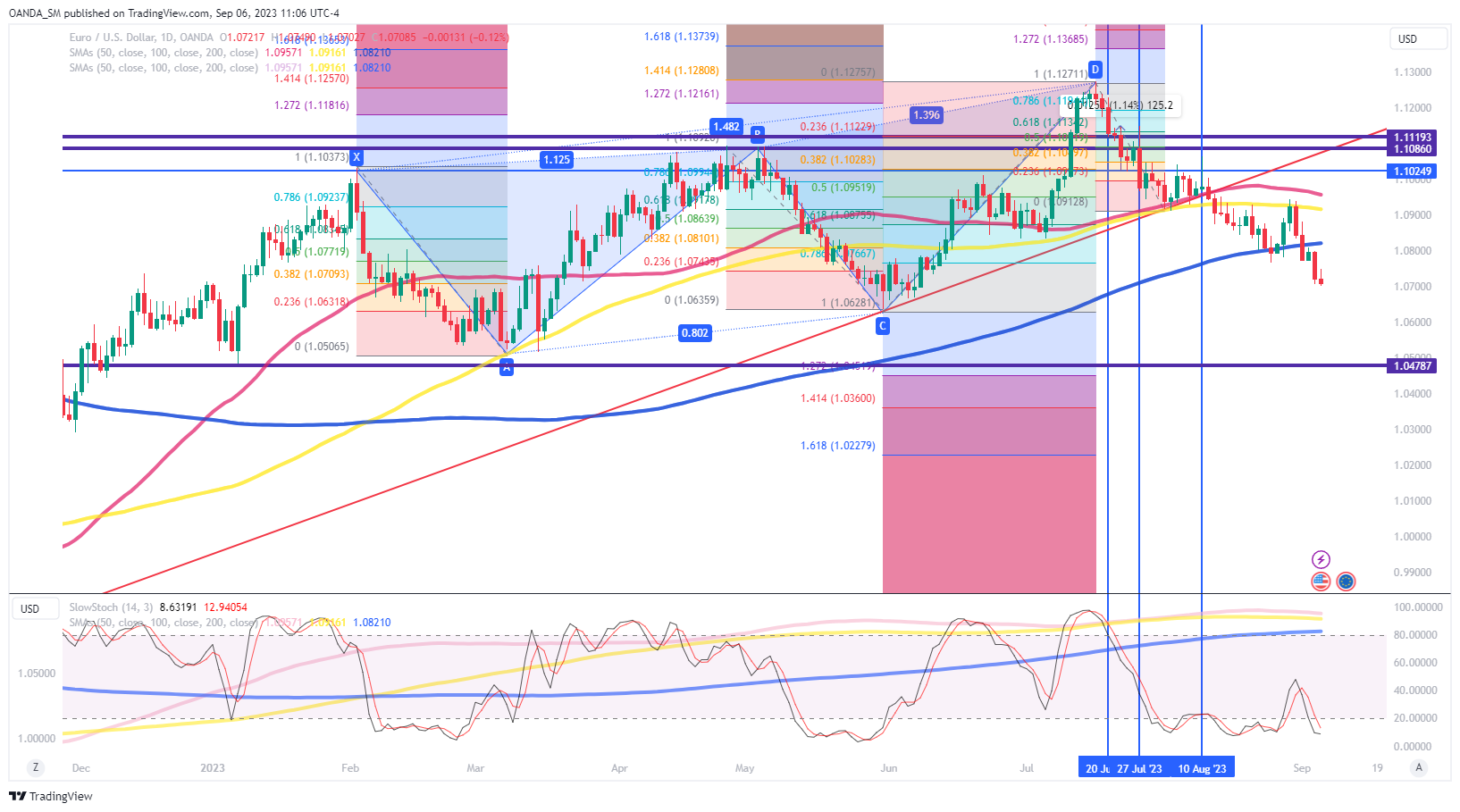

- Euro looks vulnerable to lose all of 2023 gains

The dollar’s rise is starting to unnerve everyone. Last night, both Japanese and Chinese officials attempted to thwart the greenback’s rally, but weren’t effective. The ECB is also trying to talk up the odds of a September rate hike, but disastrous German factory order data reminded us how bad of shape the eurozone’s largest economy is in. The king dollar trade has returned over the past month and half as the US growth exceptionalism trade appears to be firmly in place. Today’s ISM service report was a strong reminder that US economic outperformance will easily be the theme in Q3.

The August ISM Service Index was so impressive that Fed rate hike expectations for the November should become a coin flip. US service sector activity jumped from 52..7 to 54.5, better than all forecasts and a six-month high. What will draw lots of attention are the components. Prices paid increased from 56.8 to 58.9. The employment component popped from 50.7 to 54.7, which was the highest reading since November 2021. New orders rose from 55.0 to 57.3. The service sector is still performing well and that should cement expectations for Q3 GDP growth north of 5.0%. The growth behind entertainment & recreation, and accommodation & food services won’t last into Q4 but expectations should remain for the largest part of the economy to stay in expansion territory.

This data doesn’t support the stance that the Fed is likely done and that could mean the US dollar might have a chance to recover all of its earlier losses from the beginning of the year.

Many traders woke up to several comments from key central bank figures, but FX talk is cheap if it is doesn’t come with convincing data/market conditions that supports decisive and meaningful action. The ECB will struggle to convince markets they can hike into a deteriorating outlook. Japanese officials are still only about halfway through their best verbal intervention threats. A gradual declining yuan is not China’s biggest problem, the property crisis and contagion risks are getting too very uncomfortable levels. If the US data stays hot, the dollar momentum could easily remain in place.

EUR/USD Daily Chart

EUR/USD has continued its significant bearishness that has been in place mid-July, which was when recession fears for the US started to ease. The swift and substantial breakdown of the May 31st low, could trigger momentum selling that targets the 1.05 handle. Exhaustion might settle for dollar strength until we get beyond next week’s ECB policy decision.

Eurozone

German factory orders were disastrous in July, a plunge of 11.7%, much worse than the expected 4.3% drop, and near some of the depressed levels seen at the peak of the pandemic. A decline was expected as the prior month was supported by robust air and spacecraft manufacturing. In the industrialized world, Germany has been in the doghouse most of this year and it seems it won’t be getting better anytime soon. Germany is likely facing a rough Q3 as China’s woes are not going to be getting better anytime soon, surging oil prices are here to stay, and as impact of the ECB’s tightening cycle is felt throughout the economy.

Despite all the doom and gloom, ECB officials are trying to convince FX markets that they might still be in a position to deliver more tightening next week. ECB’s Kazimir said that a September rate hike is preferable than doing one later. ECB’s Knot also warned that markets might be underestimating the odds that they will raise rates next week. The euro pared losses following the hawkish ECB comments, but the bearish trend appears to still be intact.

Japan

Last night, Japan’s top currency diplomat Kanda reiterated the stance that FX moves should reflect fundamentals and that he was seeing speculative moves and would not rule out any options. We have heard a lot from the vice-minister of finance for international affairs, and the markets aren’t really believing Japan is close to delivering on these threats.

The yen is at a 10-month low against the dollar and much closer to the critical levels that triggered intervention last year. The comments out of Japan clearly are showing the discomfort with officials, but are still not quite at the tipping point for actually intervening.

Actual intervention will be more likely if dollar-yen is above 150 and officials are stating that they are ‘ready to take action at any time’ or if they state that it is ‘fine to consider us on standby.’

China

After falling to a 10-month low, China’s major state-owned banks were seen withdrawing yuan liquidity in the offshore FX market, which makes it more expensive to short the yuan. China’s state banks are known to do the work for the PBOC, but the current actions aren’t significant enough to put an end to the weakening yuan trend. China’s growth trend is not going to get better anytime soon, so authorities might not be as aggressive in defending the yuan. The focus for Chinese officials will be to contain the deepening property market crisis.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- ChartPrime. Elevate your Trading Game with ChartPrime. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://www.marketpulse.com/newsfeed/eur-usd-shrugs-off-hawkish-ecb-speak-dollar-firms-after-impressive-ism-services-report/emoya