(Last Updated On: August 23, 2023)

Do You Have To Pay Taxes On Crypto? The answer is yes! Just like any other form of income or investment, cryptocurrencies are subject to taxation. But fear not, because in this blog post, we’ll explore how taxes are calculated on cryptocurrency and most importantly, how you can reduce them. So grab your virtual wallets and let’s dive into the fascinating world of crypto taxes!

How are taxes calculated on cryptocurrency?

When it comes to cryptocurrency, taxes can be a bit of a gray area. The digital nature of cryptocurrencies like Bitcoin and Ethereum has made it difficult for governments to establish clear guidelines on how they should be taxed. However, that doesn’t mean you’re off the hook when it comes to paying taxes on your crypto earnings.

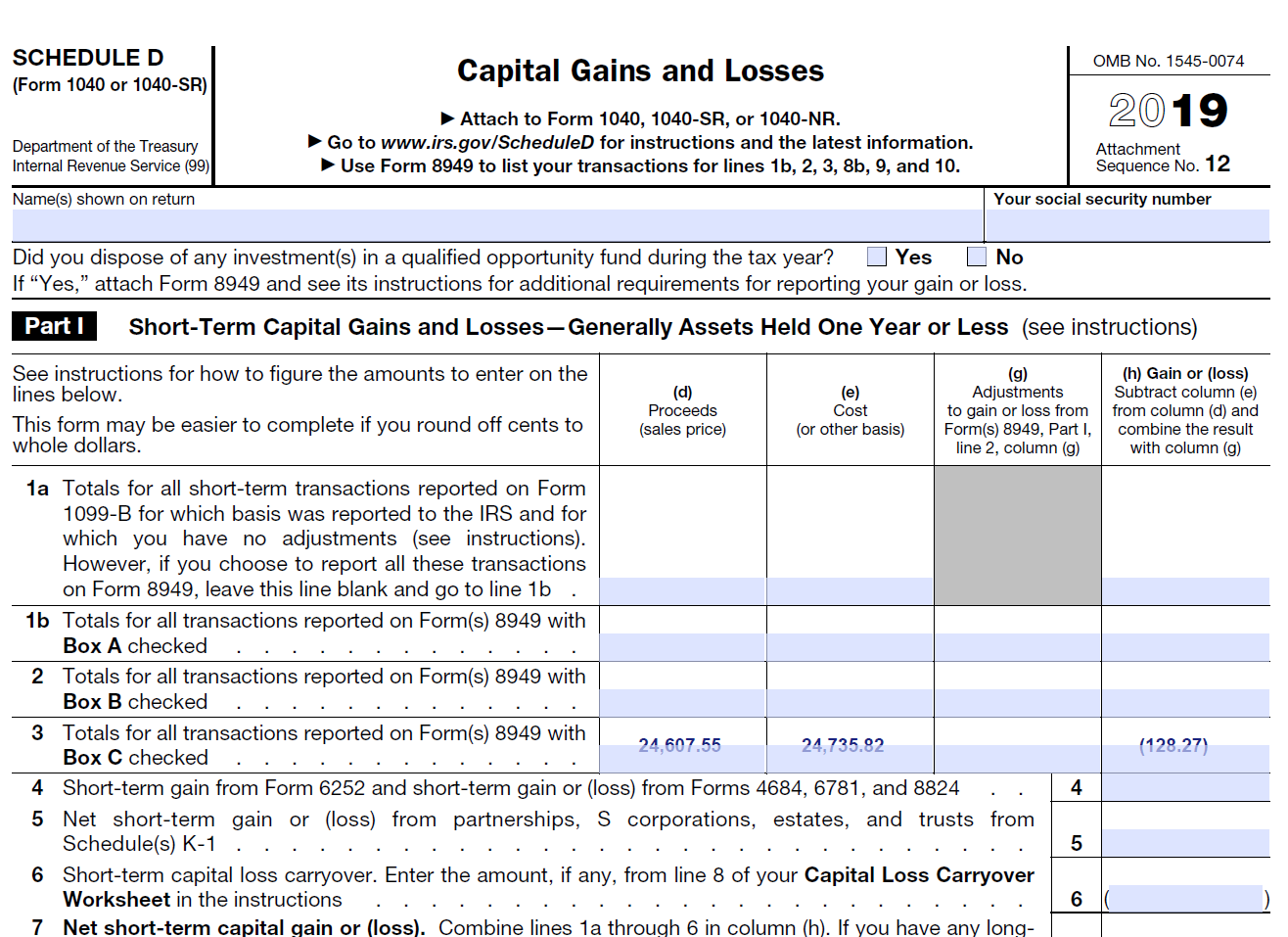

So, how are taxes calculated on cryptocurrency? Well, it largely depends on the country you reside in. In the United States, for example, the Internal Revenue Service (IRS) treats cryptocurrencies as property rather than currency for tax purposes. This means that every time you buy or sell a cryptocurrency, whether that’s trading one crypto for another or using it to purchase goods or services, you need to report any gains or losses.

Calculating your taxable income from crypto can get quite complicated since each transaction needs to be documented and its value converted into USD at the time of transaction. Additionally, if you mine cryptocurrencies as part of your income stream or receive them as payment for services rendered, those earnings are also considered taxable income.

To determine your tax liability accurately and ensure compliance with relevant regulations, seeking professional advice from accountants who specialize in cryptocurrency taxation is highly recommended. They have expertise in navigating complex tax laws related to digital assets and can help minimize your liabilities while keeping everything above board.

Remember that failing to report taxable transactions could result in penalties or even legal consequences down the line. So always err on the side of caution by properly documenting all crypto-related activities and consulting with experts when needed.

It’s worth noting that there are different strategies available to reduce taxes on cryptocurrency holdings legally. These strategies include holding assets long-term (more than one year), utilizing capital loss deductions against other forms of capital gains (stocks or real estate), contributing funds into retirement accounts known as self-directed IRAs through rollovers from existing traditional IRAs or 401(k)s; these contributions may provide immediate tax benefits such as deferring taxes or even tax-free growth until distributions are taken in retirement.

What are the different ways to reduce taxes on cryptocurrency?

When it comes to cryptocurrency, taxes can be a complex and confusing topic. However, there are several strategies you can implement to help reduce your tax liability and keep more of your crypto earnings in your pocket.

One way to potentially reduce taxes on cryptocurrency is through the concept of tax-loss harvesting. This involves selling off investments that have decreased in value to offset any gains you may have made throughout the year. By strategically timing these sales, you can minimize your overall taxable income.

Another strategy to consider is using a self-directed IRA or 401(k) account to invest in cryptocurrencies. By doing so, you may be able to defer paying taxes on any gains until retirement when you are likely in a lower tax bracket.

Additionally, if you engage in frequent trading or investing activities, it’s important to keep detailed records of all transactions. This will not only help ensure accurate reporting but also provide evidence for any deductions or exemptions that may apply.

Furthermore, consulting with a knowledgeable CPA or tax professional who specializes in cryptocurrency taxation can be invaluable. They can offer guidance on specific deductions and credits available for crypto investors as well as navigate the ever-changing landscape of crypto regulations.

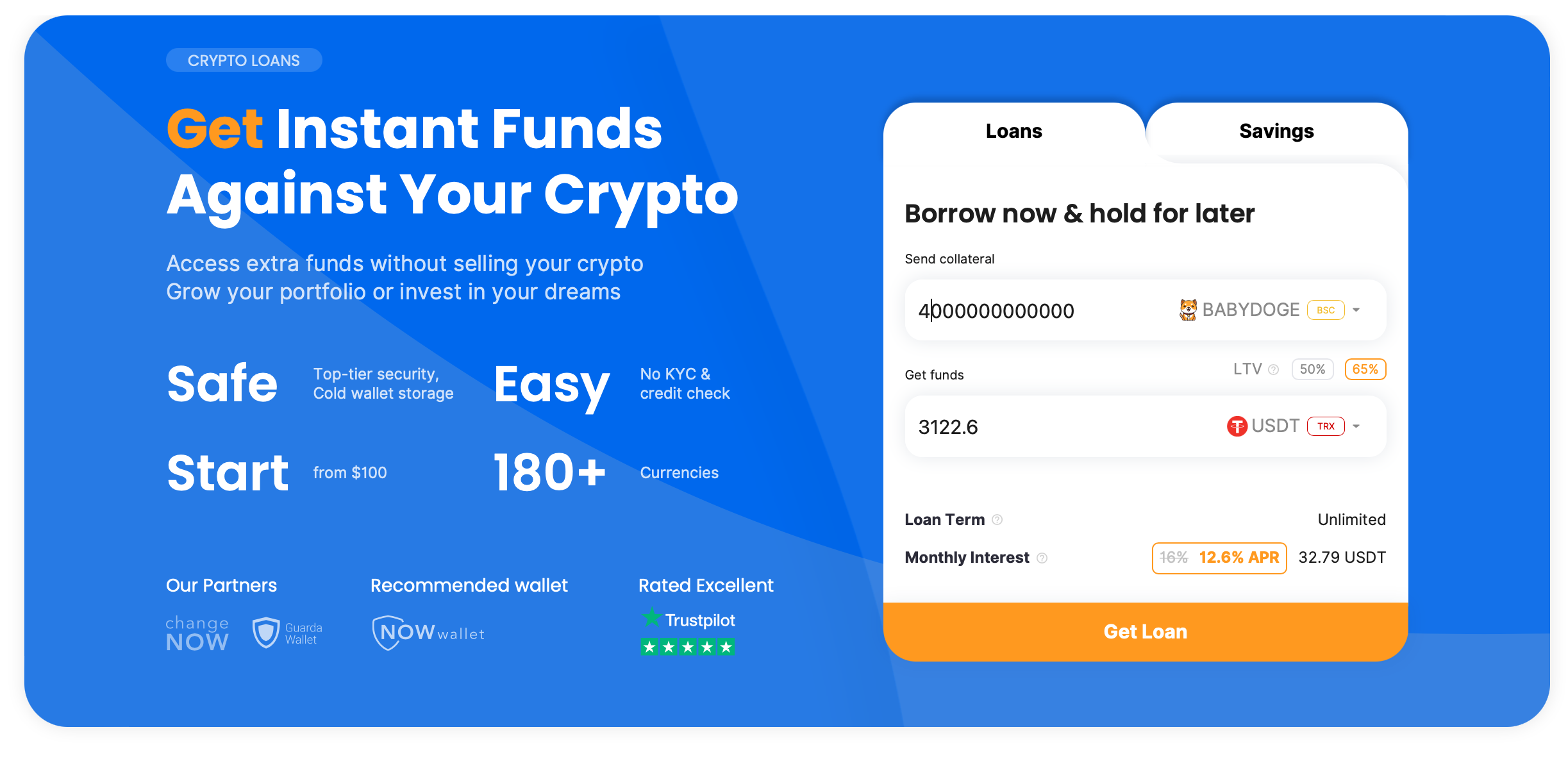

Utilizing specialized tools like CoinRabbit can help maximize your tax efficiency. Getting a crypto loan and its spending – are non-taxable events, because they do not generate direct earnings.

How to use CoinRabbit to optimize crypto taxes?

Crypto lending platforms can be a powerful tool for crypto investors looking to reduce their tax burden. By utilizing these platforms, investors can generate passive income from their holdings while also potentially offsetting capital gains taxes.

To get started, investors simply deposit their cryptocurrencies into the lending platform and select the loan terms that best suit their needs. The platform then matches them with borrowers who are willing to pay interest on these loans. This allows investors to earn additional income on top of any price appreciation in their crypto assets.

One of the key advantages of using crypto lending platforms is that they provide an opportunity for tax optimization. Instead of selling your crypto assets and triggering taxable events, you can lend them out and receive interest payments instead. Since interest income is generally taxed at a lower rate than capital gains, this strategy can help reduce your overall tax liability.

Additionally, some lending platforms offer specific features designed to minimize taxes further. For example, certain platforms may allow you to reinvest your earned interest directly into new loans or other investment products within the platform without triggering a taxable event.

It’s important to note that while using crypto lending platforms can have significant tax benefits, it’s crucial to consult with a qualified tax professional before implementing any strategies. Tax laws vary by jurisdiction and there may be specific rules or regulations that could impact your individual situation.

Incorporating crypto lending platforms into your investment strategy can be an effective way to reduce taxes while generating passive income from your cryptocurrency holdings. By taking advantage of these innovative tools and working closely with professionals who specialize in cryptocurrency taxation, you’ll be well-positioned to navigate the complex world of crypto taxes successfully

Conclusion

As the popularity and usage of cryptocurrencies continue to grow, it is important for crypto holders to understand their tax obligations. While taxes on cryptocurrency can be complex and confusing, there are various strategies that can help reduce your tax liability.

Make sure you accurately calculate your capital gains or losses from cryptocurrency transactions. Keep detailed records of all your transactions and consult with a tax professional if needed.

Additionally, take advantage of any available deductions or credits related to cryptocurrencies such as mining expenses or transaction fees. Consult with a qualified accountant who specializes in cryptocurrency taxation to ensure you are maximizing these opportunities.

Consider using CoinRabbit’s services to optimize your crypto taxes. With their innovative platform and expert team, they can provide personalized advice tailored to your specific situation. By taking advantage of CoinRabbit’s tools and guidance, you can minimize your tax liability while remaining compliant with the law.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- ChartPrime. Elevate your Trading Game with ChartPrime. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://coinrabbit.io/blog/do-you-have-to-pay-taxes-on-crypto/