- USD/JPY rallied by 100 pips and broke above 142.50 resistance in yesterday’s NY session.

- Japan’s headline inflation for May softened but the core-core rate (excluding fresh food & energy) accelerated to 4.3% y/y, a 42-year high.

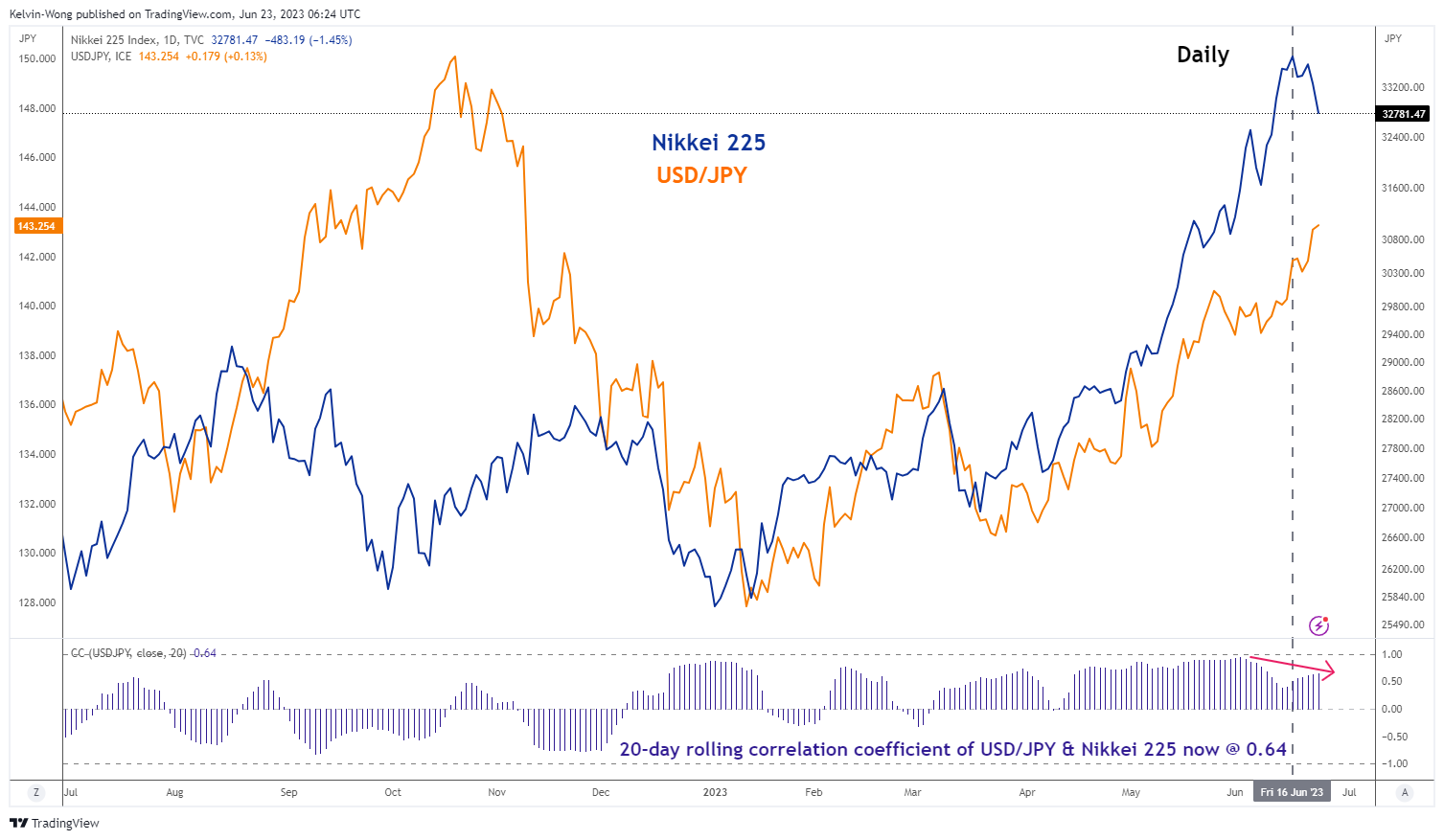

- High direct correlation between USD/JPY & Nikkei 225 has dissipated.

- Watch the next key resistance zone of 145.50/146.10 for USD/JPY.

In a stunning move, the USD/JPY has rallied by 100 pips from the start of yesterday, the 22 June US session to print an intraday high of 143.23, a level that was last seen in November 2022.

This current bout of JPY weakness has been reinforced by the breakout of a key 142.50 medium-term resistance on the USD/JPY but was not supported by any fresh economic data or event catalyst yesterday. The tonality of the delivery, as well as the questions and answers session for Fed Chair Powell’s second round of congressional semi-annual testimony yesterday on the current state of the US economy and Fed’s monetary policy stance, was the same rhetoric as the first round of testimony delivered earlier on Wednesday, 21 June.

Strong USD/JPY could be due to month-end and quarter-end flows

Thus, yesterday’s strong push-up in the USD/JPY could be related to month-end and quarter-end flows where next week will be the last for June and Q2 2023 as well as some form of anticipation of the outcome of key economic data on Japan that was due this morning, Asian session; inflation for May and flash Manufacturing and Services Purchasing Managers’ Indexes (PMI).

Elevated sticky inflation data while manufacturing activities contracted again

Japan’s headline inflation rose at a slower pace in May, 3.2% year-on-year from April’s three-month high of 3.5%, which also came in below expectations of 4.1%. The core inflation rate (excluding fresh food) also inched lower to 3.2% year-on-year in May from 3.4% in April but managed to beat expectations of 3.1% and remained above Bank of Japan (BoJ)’s 2% target for the 14th consecutive month.

Most importantly, the core-core inflation rate (excluding fresh food & energy), a key barometer of underlying domestic demand-driven price trends continued to accelerate in May and hit a 42-year high of 4.3% year-on-year over April’s print of 4.1%.

These latest inflationary trends out from Japan suggest that sticky inflation that excludes fresh food and energy has continued to grow and remains at an elevated level that runs counter to the latest BoJ’s guidance (from last Friday’s monetary policy decision) that insisted that inflation growth in Japan was at risk of falling in the second half of the current fiscal year.

Thus, the next BoJ’s monetary policy decision in July will be closely watched as it also released its latest quarterly outlook which includes growth and inflation forecasts to see whether BoJ will start to sway away from its ultra-easy monetary policy stance.

Next Friday, 30 June, we will have the Tokyo area inflationary data for June which tends to be a leading indicator for the nationwide inflation trend.

A few economic growth concerns over here as the flash Manufacturing PMI for June hit a contraction mode again of 49.8 after it expanded to 50.6 in May, its highest reading in seven months. In addition, the services sector grew at a slower pace in June where the flash Services PMI came in at 54.2 from 55.9 in May, and below expectations of 56.2.

A weaker JPY does not translate to risk-on behaviour in Nikkei 225 for now

Fig 1: 20-day rolling correlation coefficient trend of USD/JPY & Nikkei 225 as of 23 Jun 2023 (Source: TradingView, click to enlarge chart)

Based on past historical trends, the movement of the Nikkei 225 and the USD/JPY tends to have a high direct correlation level as a weaker JPY (USD/JPY strengthening) tends to fuel risk-on behavior via the carry trade factor as JPY is mostly used as a global funding currency due to its negative interest rate.

Interestingly, this initial high direct correlation between the USD/JPY and Nikkei 225 has started to dissipate in the past two weeks since the Nikkei 225’s steep bull run from March 2023 low hit a 33-year high of 33,772 earlier this month, June.

The 20-day rolling correlation coefficient has fallen to 0.63 from a high of 0.94 printed on 2 June 2023 and the level of around 0.90 was the average for the last three months.

Hence, it seems that the current weakness seen in the Nikkei 225 for the past five days (-3.22% from the 19 June high) has ignored the ongoing rally in USD/JPY (carry trade factor) but rather moved in synch with the current soft footing seen in global equities.

Based on this current week-to-date time frame, major stock indices have declined due to a higher for longer period of interest rates mantra from the Fed and other G-20 central banks (ECB, BoE, BoC); S&P 500 (-0.63%), Nasdaq 100 (-0.28%), STOXX Europe 600 (-2.6%), Hang Seng Index (-6%), and Hang Seng China Enterprises Index (-6.8%) at this time of the writing.

Momentum remains bullish for USD/JPY but watch out for risk aversion & BoJ intervention

Fig 2: USD/JPY medium-term trend as of 23 Jun 2023 (Source: TradingView, click to enlarge chart)

Technical analysis is suggesting the medium-term uptrend phase of the USD/JPY remains intact since the 16 January 2023 low of 127.22 with the next key resistance zone coming in at 145.50/146.10.

The daily RSI is overbought but has no bearish divergence and has yet to hit an extreme overbought level of 78.90 which has led to a prior significant decline in USD/JPY after its 21 October 2022 swing high. These observations suggest upside momentum remains intact at this juncture.

Two key scenarios may derail this bullish run in USD/JPY. Firstly, global equities especially, the outperforming US mega-cap technology group fuelled by the Artificial Intelligence (AI) growth narrative continue to see further declines which may trigger a bout of risk-averse behavior that tends to see a revival of JPY strength which has occurred in the past.

Secondly, Japan’s Ministry of Finance officials and politicians may start to get “uncomfortable” with the swift up move of USD/JPY and put pressure on BoJ to intervene. Last week, Chief Cabinet Secretary Hirokazu Matsuno commented that excessive movements in the foreign exchange market were not desirable which echoed similar statements made by Vice Finance Minister, Masato Kanda, a top currency official on 30 May.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Latest posts by Kelvin Wong (see all)

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://www.marketpulse.com/forex/usd-jpy-surged-to-a-7-month-high-but-fundamentals-diverge/kwong