Executive Summary

- The introduction of Ethereum’s staking withdrawal functionality in mid-April has sparked a surge in interest for liquid staking tokens.

- Among liquid staking providers, Lido has established overwhelming dominance, boasting the highest supply, liquidity, and integration network effects, all of which solidify its position in the market.

- A new trend has evolved in regard to the DeFi integration of liquid staking tokens. Liquidity pools associated with liquid staking are witnessing a decline in locked value, as capital migrates towards use as collateral in lending protocols.

Relative Performance

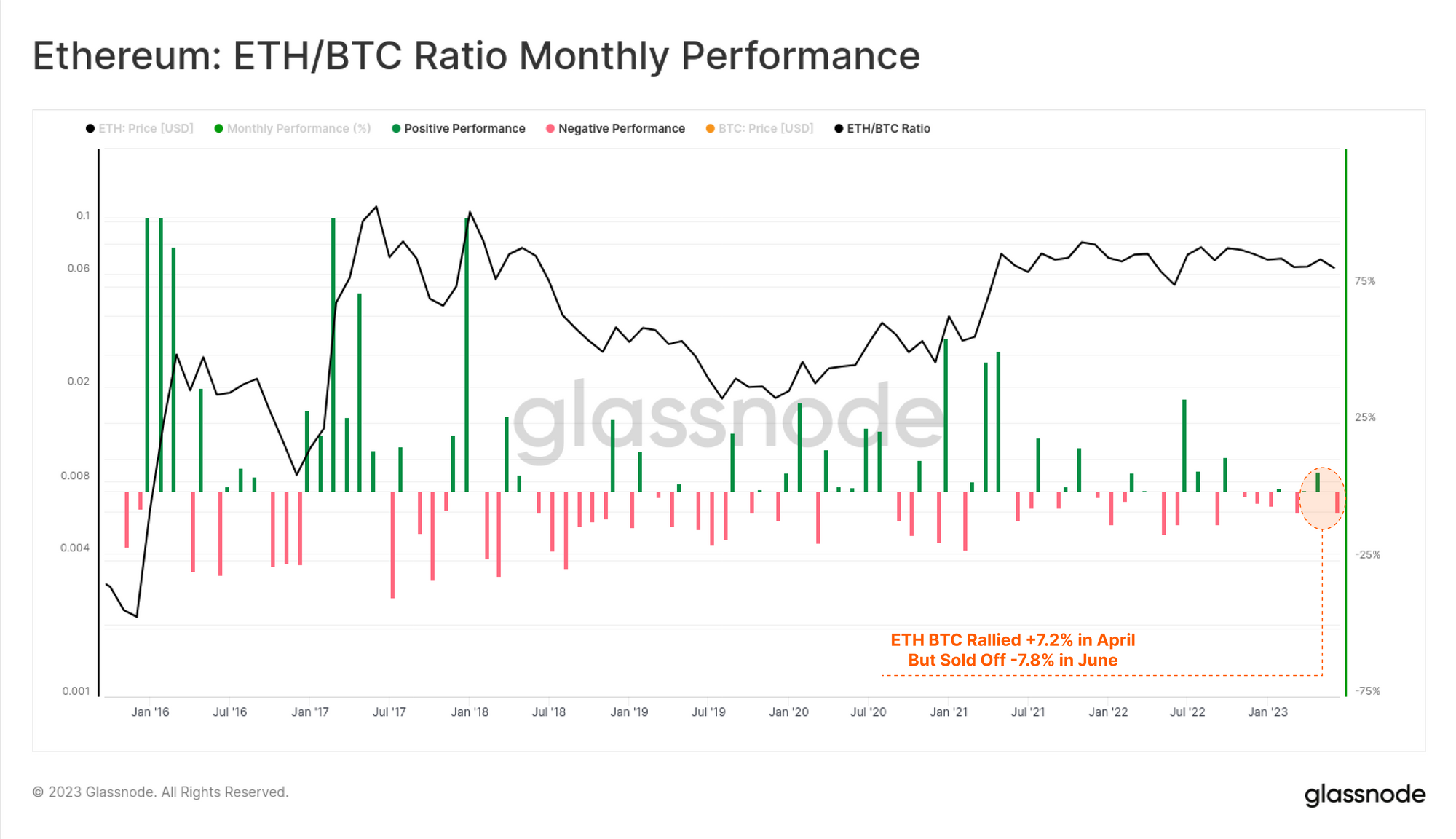

The digital asset market has been processing the slew of spot BTC ETF applications over recent weeks, with notable BTC out-performance relative to the rest of the market. Whilst the ETF filing by BlackRock initially lifted The ETH price by 11.2%, it has closed Q2 a surprisingly quiet 6.4% above its April open.

On a relative basis, many digital assets have lost ground against Bitcoin in 2023, with the ETH/BTC ratio sliding down to a 50-week low of 0.060. This ratio has rallied back to 0.063 however, showing some strength into the start of July.

📈

Thus far in 2023, the uptick in ETH prices have not yet translated into significantly increased network activity. Gas prices, which are considered a proxy for blockspace demand, have remained relatively low, especially in the week following the ETF filing announcements. For comparison, during the Shanghai upgrade in April, which preceded a similar rally in ETH markets, gas prices rose by 78%, compared the the 28% this week.

Waves of New Staking Deposits

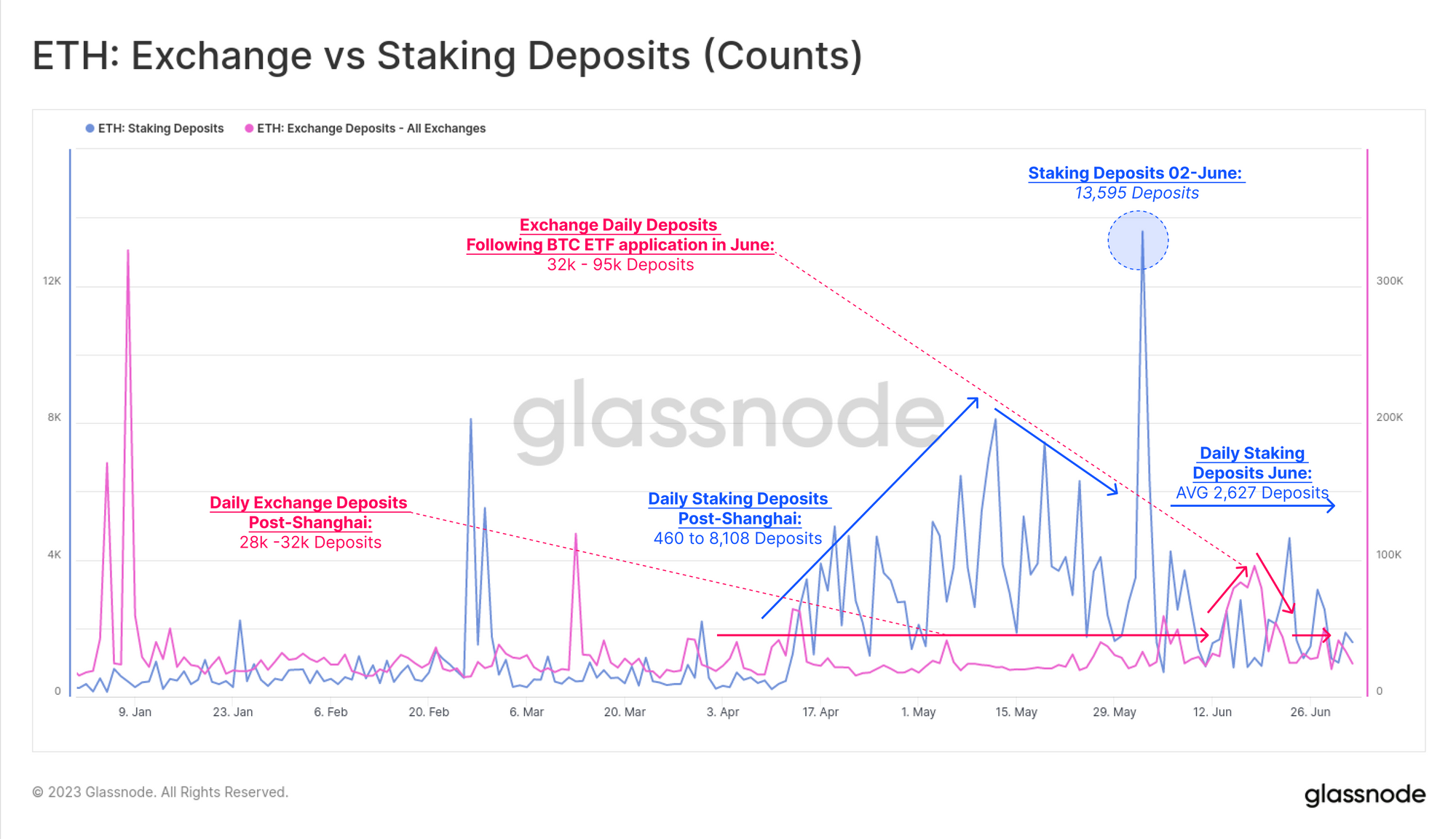

The Shanghai hardfork enabled staked ETH to be withdrawn from the Ethereum consensus mechanism. Rather than seeing a wave of withdrawals however, instead the upgrade has motivated a fresh wave of deposits, as stakers find confidence in this new flexibility.

Deposit activity (transaction counts) reached a peak on 2-June, recording over 13,595 new deposits (worth over 408k ETH). For comparison, we can compare this to ETH exchange deposit transactions, which have remained flat at around 30k deposits transactions over this period.

The burst of new staked ETH is even clearer if we compare ETH volume staked (blue) vs exchange inflow volume (red). Newly staked ETH has been higher, or equal in scale to exchange inflows since Shanghai went live.

Upon closer examination, we can isolate daily deposits by provider, where a very clear trend in favor of liquid staking providers becomes evident, with Lido is leading this trend.

Lido Dominance

The above observations reflect a market demand for liquid staking tokens (LSTs). These tokens are effectively a wrapper for ETH deposited into the staking pool, with the staking operations abstracted away from the end user by the platform.

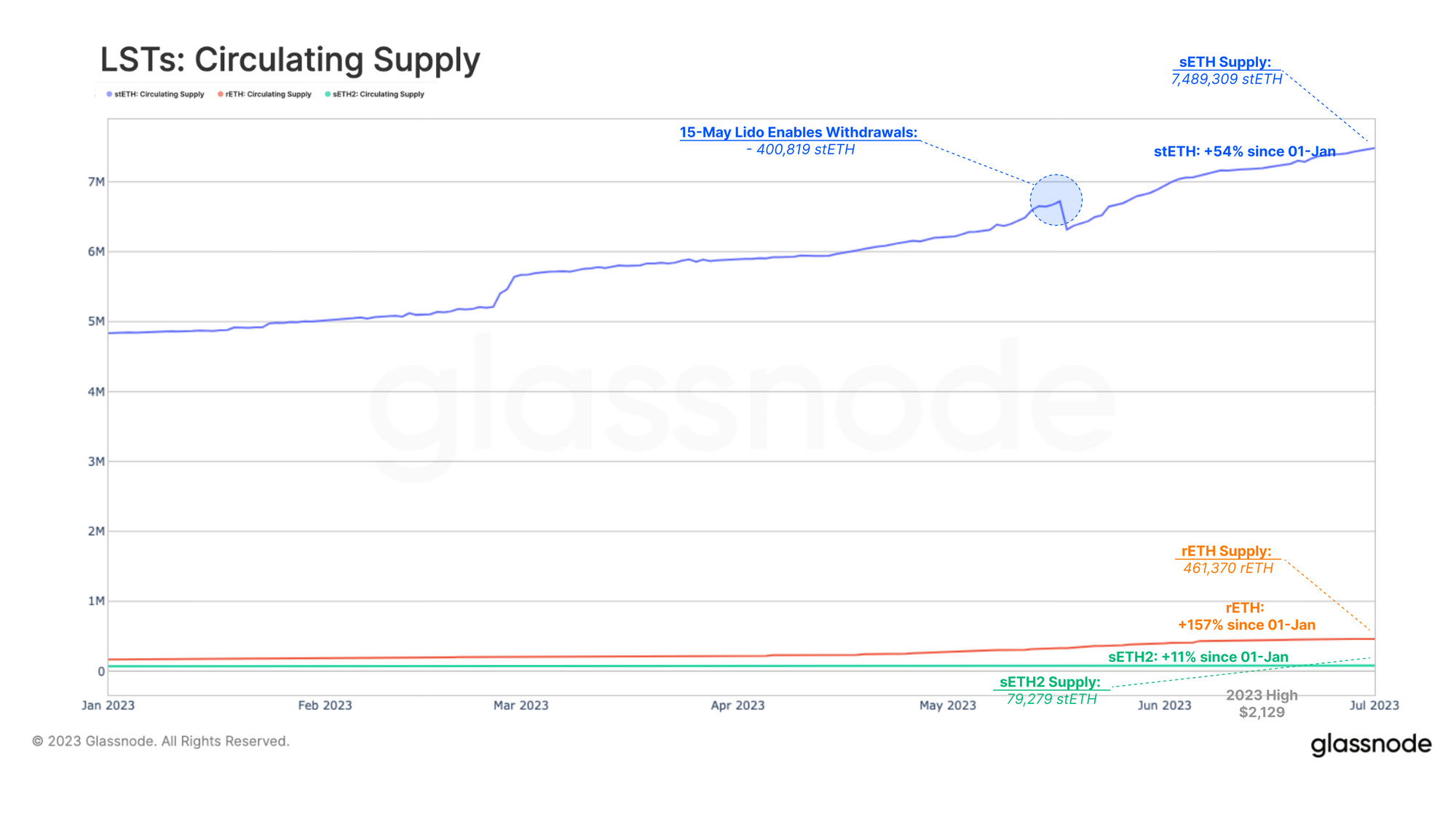

Lido released its V2 update on 15-May which allowed node operators to withdraw staked ETH, enabling holders of Lido’s stETH token to exchange it for ETH. Following the release, there was a redemption of 400k stETH ($721M), resulting in a contraction of the stETH supply. However, the huge wave of new ETH deposits have more than compensated the decline, pushing to a new ATH of 7.49M stETH.

When comparing to other liquid staking competitors, Lido stands out as the clear leader in the sector with its supply 16 times higher than its nearest competitor. That said, the supply of rETH, which is the liquid staking token of Rocketpool, has been growing three times faster than Lido’s since the beginning of this year.

Interestingly, the increasing demand for Lido’s stETH is not reflected in an increasing number of new token holders. While we observe an increase in users of the staking tokens of Rocketpool and FRAX after the Shanghai upgrade, Lido has not registered a significant growth in new users.

New addresses holding stETH is oscillating between 230-590/day, which is more or less unchanged YTD. This leads us to the conclusion that many new deposits made via Lido are driven by existing stETH token holders increasing their exposure.

When looking at the average token holder balance, we can estimate how the newly issued stETH tokens have been distributed. After withdrawals were enabled for Lido, the average balance of token holders dropped to 46.1 stETH ($83k).

The average stETH balance has increased to 51.0 stETH ($100k) since Shanghai, indicating that existing token holders are indeed increasing their share of ETH staked in the form of stETH. It also suggests we are yet to see an appreciable influx of new holders entering the market via these staking mechanisms.

Shifting LST Usage in DeFi

A key value proposition of LSTs is their integration into DeFi protocols. LST token holders can easily trade LSTs on decentralized exchanges, use them as collateral, or take advantage of yield opportunities via lending protocols.

Since their inception, LSTs have seen increased activity within different DeFi protocols, with Lido’s stETH being the most significant. The network effects and integrations of stETH is another factor leading to Lido dominance in the sector. However, amongst the suite of DeFi protocols accepting LSTs, there are several interesting trends developing.

Since the Shanghai Upgrade, the stETH-ETH Curve Pool, which is the largest liquidity pool for Lido’s staking derivative, has lost 39% of its total value locked. It is now approaching the levels seen after the great deleveraging following the Terra-Luna collapse in May 2022.

Examining the wstETH-ETH Pool on Balancer, we can observe this trend is even more pronounced. Since 15-April the TVL of this pool has decreased by 71%, reducing the pool value from $351.2M to $101.4M.

By examining the annualized yield (APR) of both pools, we can see a consistent downtrend has been established in 2023. For our analysis, we take 15-April as the reference point as it is around that time when the wave of new staking deposits began, as well as the decrease in liquidity on the relevant DEXs.

The APR for the Curve stETH-ETH pool has decreased from 3.47% on April 15th to 2.27% today. On the other hand, the Balancer pool reached its lowest point of 1.69% in April and has slightly increased to 2.10% since then.

Keep in mind that APRs for liquidity pools are comprised of different reward structures paid in different tokens. The Lido project rewards Curve liquidity providers with LDO tokens on-top, with this incentive programme running out on 1-June. Given the contrasting APR trends on both platforms, this changing reward structure alone does not provide a conclusive explanation for the declining liquidity.

It may be that APRs have been rendered somewhat irrelevant for LST pools since the opening of withdrawals. Before Shanghai, liquidity pools functioned as the sole source of liquidity for stakers, however now the requirement to trade between stETH and ETH on DEXs has decreased, and users can mint or redeem directly with the platform.

This may alude to market makers seeing diminished return opportunities as DeFi liquidity providers. Moreover, this trend may have be reinforced by the retreat of several major market makers due to heightened regulatory scrutiny in the USA.

Since we do not see any sudden withdrawals of liquidity caused by the departure of a few players, but rather a continuous trend, we assume that these decreases in liquidity are likely due to more structural shifts.

Another explanation could be the increase in potential opportunity costs for liquidity providers resulting from new revenue streams across other DeFi protocols. Lending pools such as Aave or Compound which allow for LSTs can be used as collateral and leveraging them against ETH. This leveraged staking position is estimated to amplify yield by 3x.

Aave has seen an appreciable increase in TVL, especially for wstETH within the V3 lending pool. Since its launch in late January 2023, the wstETH pool has swelled to over S734.9M in value, whilst the stETH pool is hovering around $1.79B.

The Compound V3 wstETH pool has also seen significant growth since its launch earlier this year, now holding over $42.2M worth of stETH. This is an increase of 817% since 9-May alone. Yield-bearing staking derivatives appear to be becoming a more attractive collateral relative to ETH and even stablecoins.

Summary and Conclusion

The Ethereum Shanghgai upgrade was completed in mid April, allowing investors to complete the withdrawal leg of the staking yield trade. Rather than witnessing a wave of withdrawals, deposits accelerated, with a very clear market preference for liquid staking tokens emerging.

Of these, Lido has captured by far the largest market share, accounting for 7.5M in staked ETH. Lido’s stETH also has network effects within the DeFi sector, being integrated and adopted as a preferred source of collateral. Since Shanghai, there has been a notable shift in stETH capital allocation within the DeFi sector, with DEX liquidity pools shrinking, and collateral usage within in lending protocols rising.

This suggests that investors may be playing a staking yield maximising strategy, building up stETH exposure via borrowed leverage to amplify returns.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Automotive / EVs, Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- BlockOffsets. Modernizing Environmental Offset Ownership. Access Here.

- Source: https://insights.glassnode.com/the-week-onchain-week-27-2023/