Aligning with global trends, Southeast Asian tech investments recorded a considerable decline in 2023, influenced by increasing interest rates, high inflation and supply chain disruption. Despite the notable pullback, fintech continued to see traction from investors, with digital lending in particular witnessing an uptake.

New reports released by Cento Ventures, a Singapore-based venture capital (VC) firm focused on technology startups, and Tracxn, a market intelligence platform, explore the state of the Southeast Asian tech investment landscape and share trends observed in the market. Among the key trends outlined in the reports, the companies note a sizable decline in tech investment volumes, adjustments in valuations and a shift towards earlier stage startups. The reports also highlight the continued dominance of fintech in the Southeast Asian tech investment landscape, with consumer lending emerging as a favored area of VC investment in 2023.

Fintech takes the lion’s share

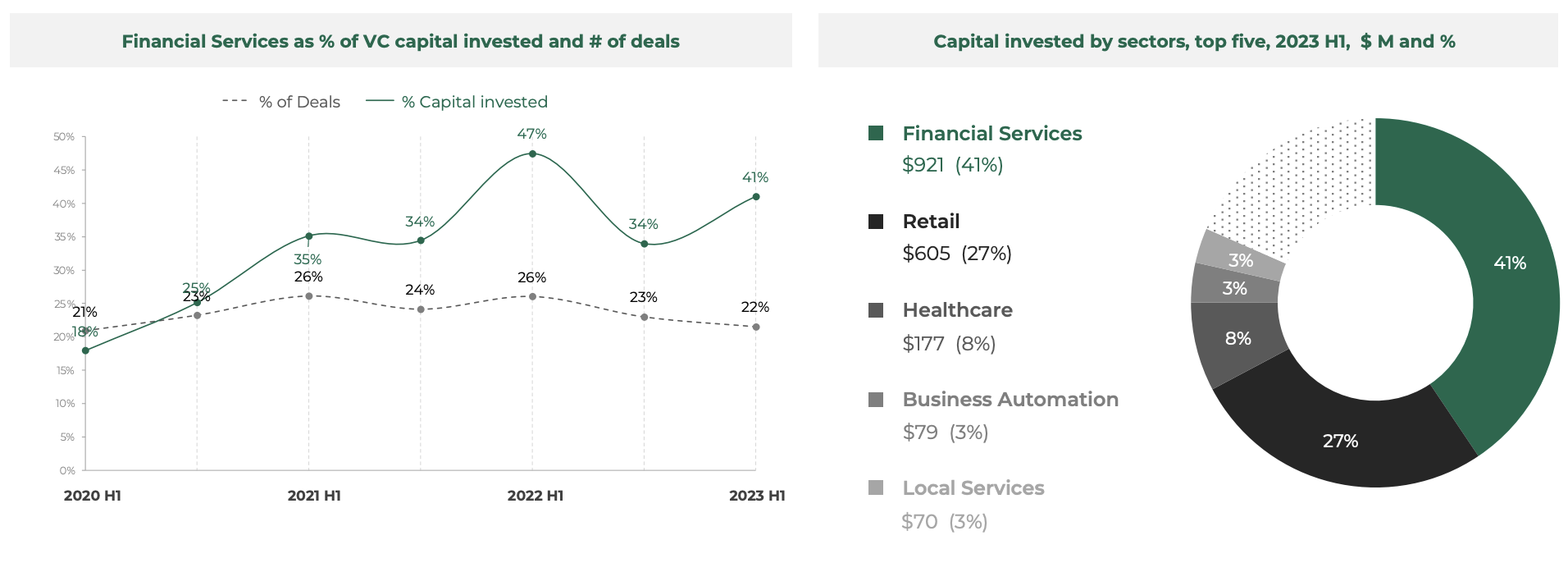

In H1 2023, digital financial services continued to lead startup investments in Southeast Asia with companies in the sector securing a total of US$921 million. The figure represents 41% of all Southeast Asian tech funding volume and makes fintech the top area of focus for investors for the period, ahead of retail (US$605 million), healthcare (US$177 million) and business automation (US$79 million).

It follows a long-lasting trend where digital financial services have consistently represented one-fifth of tech transactions in Southeast Asia, while attracting a share between 35% and 50% of invested capital.

Share of financial services as % of VC capital invested and # of deals, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

The dynamism of the fintech sector comes on the back of rapid updates to regional payment infrastructure and conducive regulations, as well as a shift of focus by industry players as they move away from the “super-app” model to favor financial services origination and distribution, Cento Ventures says.

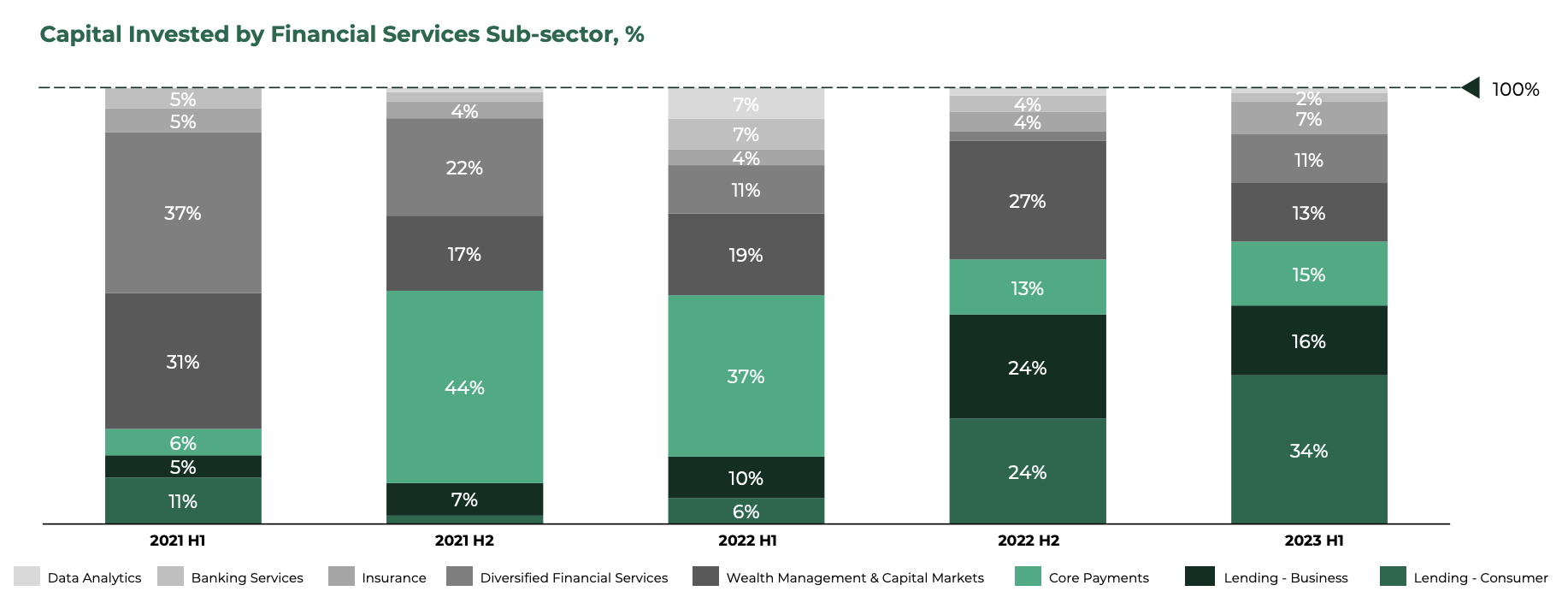

Lending segments leads, Wealthtech takes a hit

Consumer lending was the favored fintech segment in H1 2023, with startups in the sector securing 35% of all funding raised by the fintech sector during the period. It follows a trend that began in H2 2022 where consumer lending began taking the lead over core payments, a major theme in H2 2021 and H1 2022.

According to Cento Ventures, this shift can be partly explained by rising interest rates which have driven up the cost of capital, making it more expensive for lending companies to raise debt rounds and prompting them to turn to VC funding. The trend is evident by the massive US$270 million and US$100 million rounds digital lending startups Kredivo and Aspire secured during H1 2023, respectively.

At the other end of the spectrum, data show that the wealth management sector is undergoing a considerable setback, witnessing a reduction of its share in total fintech funding. In H1 2023, wealth management and capital markets startups in Southeast Asia secured 13% of all fintech funding in the region. The rate is the lowest level recorded since H1 2021 during which the sector made up 31% of all fintech funding.

According to Cento Venture, one driver of this trend is the 2022 bear market in the digital assets space and the end of cheap credit, which have decreased the demand for margin trading.

Capital invested by financial services sub-sector, %, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

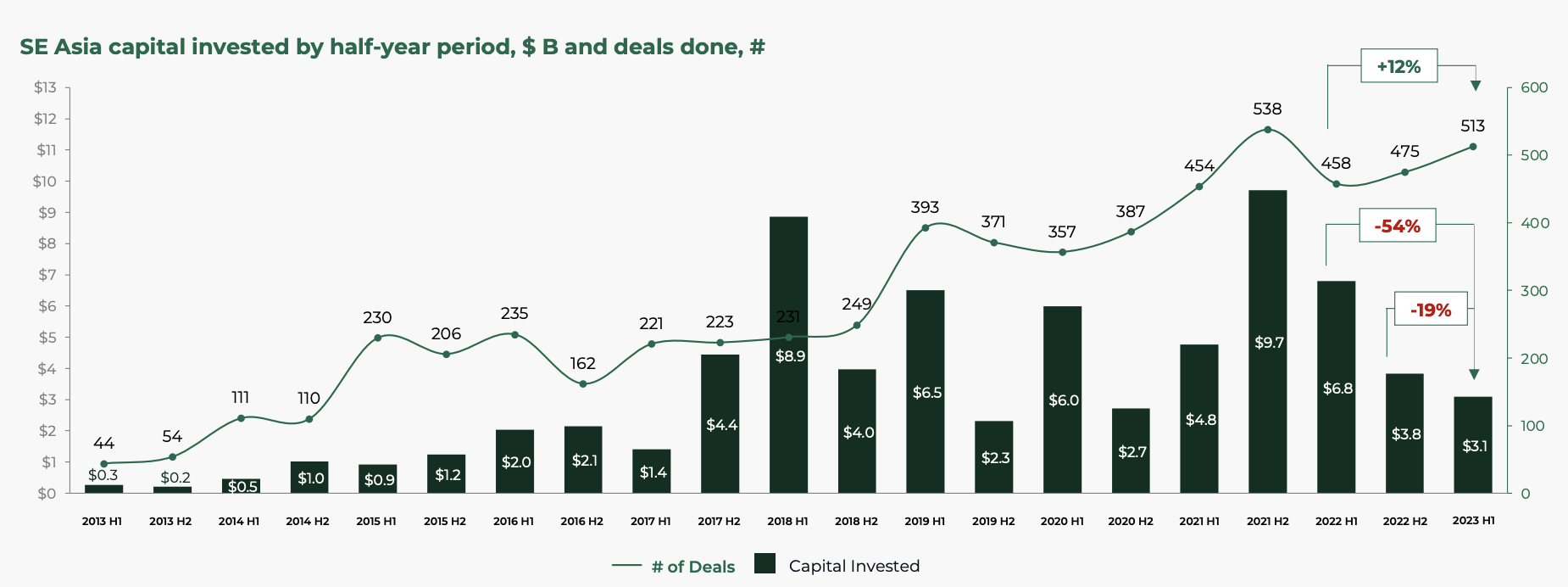

Southeast Asian tech funding drops 54% YoY

Looking at the broader tech startup landscape, the report reveals a notable pullback in VC funding. In H1 2023, Southeast Asia recorded a substantial 54% year-on-year (YoY) decline in tech investment volume which reached US$3.1 billion for the period.

The figure marks the lowest first-half investment volume since 2017 and suggests that the deal landscape may be reversing to levels observed before COVID-19, possibly even returning to standards seen before the era of unicorn startups, Cento Ventures says.

This drop was driven in part by the decline of mega-rounds of financing US$100 million and up, which carried on in H1 2023. Mega-rounds totaled a mere US$800 million in H1 2023, a stark contrast from H1 2021’s US$5.3 billion and H1 2018’s all-time high of US$7.5 billion.

Southeast Asia capital invested by half-year period, US$B and deals done, #, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

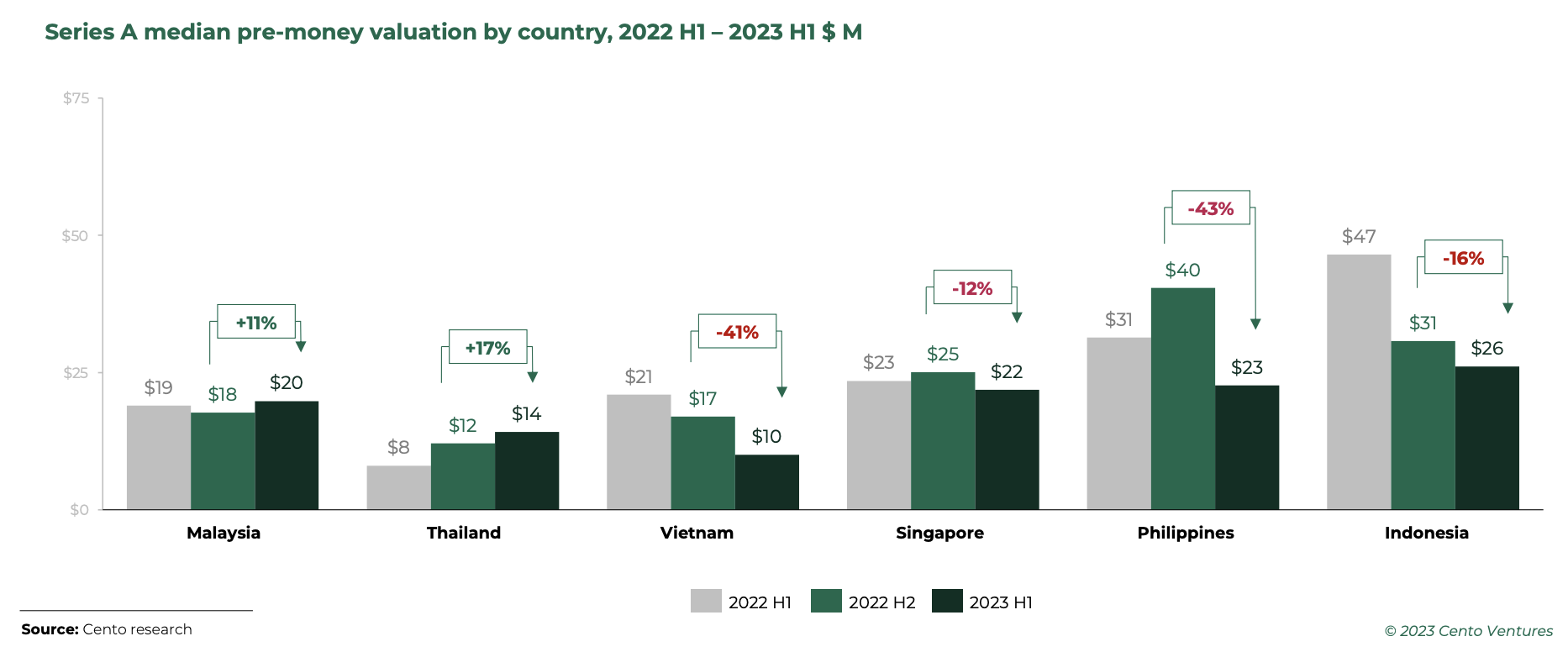

Valuations continue to adjust

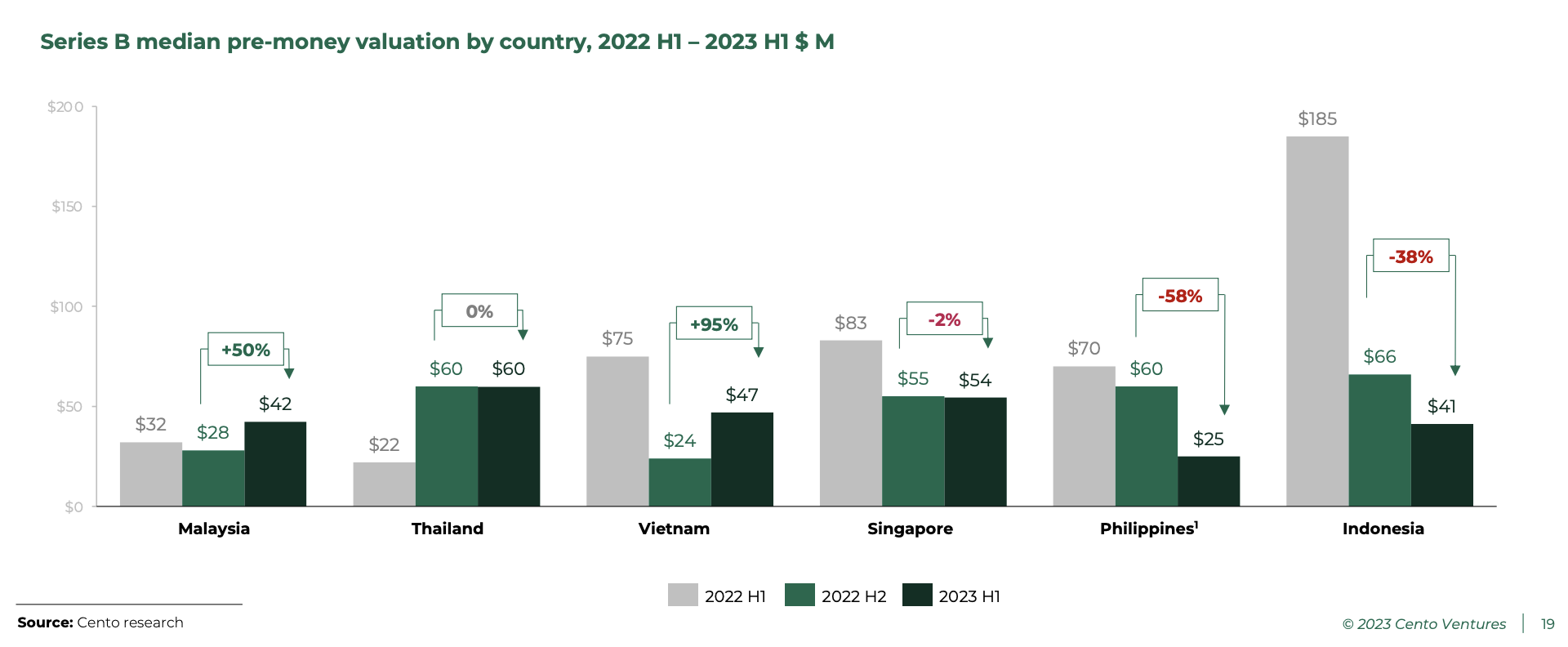

Valuations continued to adjust in H1 2023, with Series B startups experiencing the most turbulence, and Indonesia and the Philippines leading the way. Conversely, Series B startups in Malaysia and Vietnam saw their valuations rise considerably, recording a 50% and 95% increase, respectively.

In Indonesia and the Philippines, investors in Series B have grown particularly sensitive to later-stage rounds (US$50-100 million per deal), which had dried up by the first half of 2023, the report says. Consequently, valuations across Series A and B have begun to converge regionally, leading to a significant reduction in Southeast Asia’s valuation gap between markets.

Series A median pre-money valuation by country, 2022 H1 – 2023 H1 US$ million, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

Series B median pre-money valuation by country, 2022 H1 – 2023 H1 US$ million, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

Investor shift focus towards earlier startups

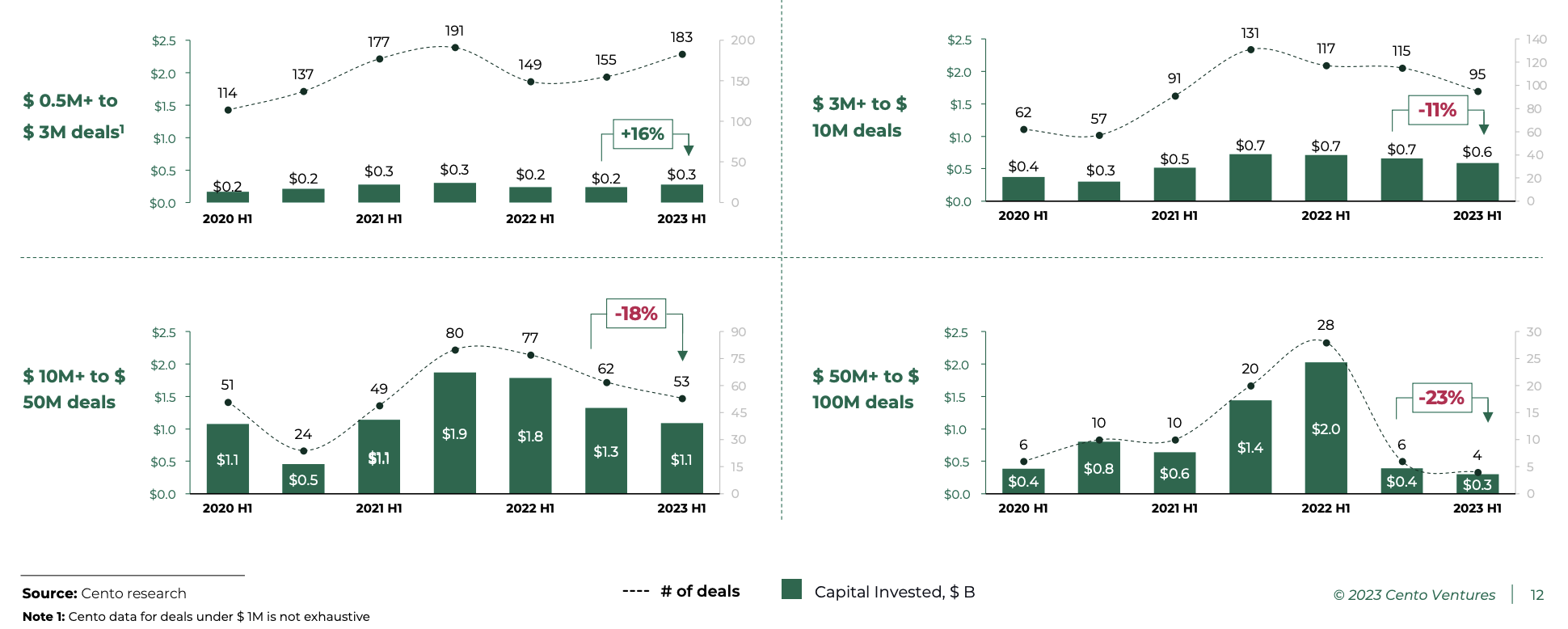

As Southeast Asia entered a period of market correction, investors continued to shift their attention towards earlier stages. In H1 2023, investments in seed and pre-Series A (US$500,000 – US$3 million) increased by 16%, following a steady trend observed over the past three years.

Series A to early Series B rounds of US$3 to 10 million continued slowing down at nearly the same rate as in the previous period, dropping by 11% between H2 2022 and H1 2023 and by 18% between H2 2022 and H1 2023, respectively.

Larger deals of US$50 million to US$100 million pulled back considerably, recording a 23% drop between H2 2022 and H1 2023. These deals totaled a mere US$300 million in H1 2023, a far cry from the US$2 billion recorded for H1 2022.

Southeast Asia tech investments by deal size, Source: Southeast Asia Tech Investment 2023 H1, Cento Ventures, Dec 2023

Antler, East Ventures most active investors in 2023

According to data from Tracxn, Antler, East Ventures and 500 Global were the three most active investors in the Southeast Asian tech scene last year, participating in 21, 17 and 10 investment deals in the region in 2023, and backing names such as Singapore payment startup Qashier, Singapore logistics startup Locad, and Indonesian e-commerce technology company Sirclo.

In the seed stage, East Ventures, Wavemaker Partners and Saison Capital were the top three investors, while Seeds, Peak XV Partners, and Gobi Partners were the most active in the early stage. In terms of late-stage funding, EDBI was the top investor by deal count with two transactions in the region last year, including Engine Biosciences’ US$27 million Series A extension.

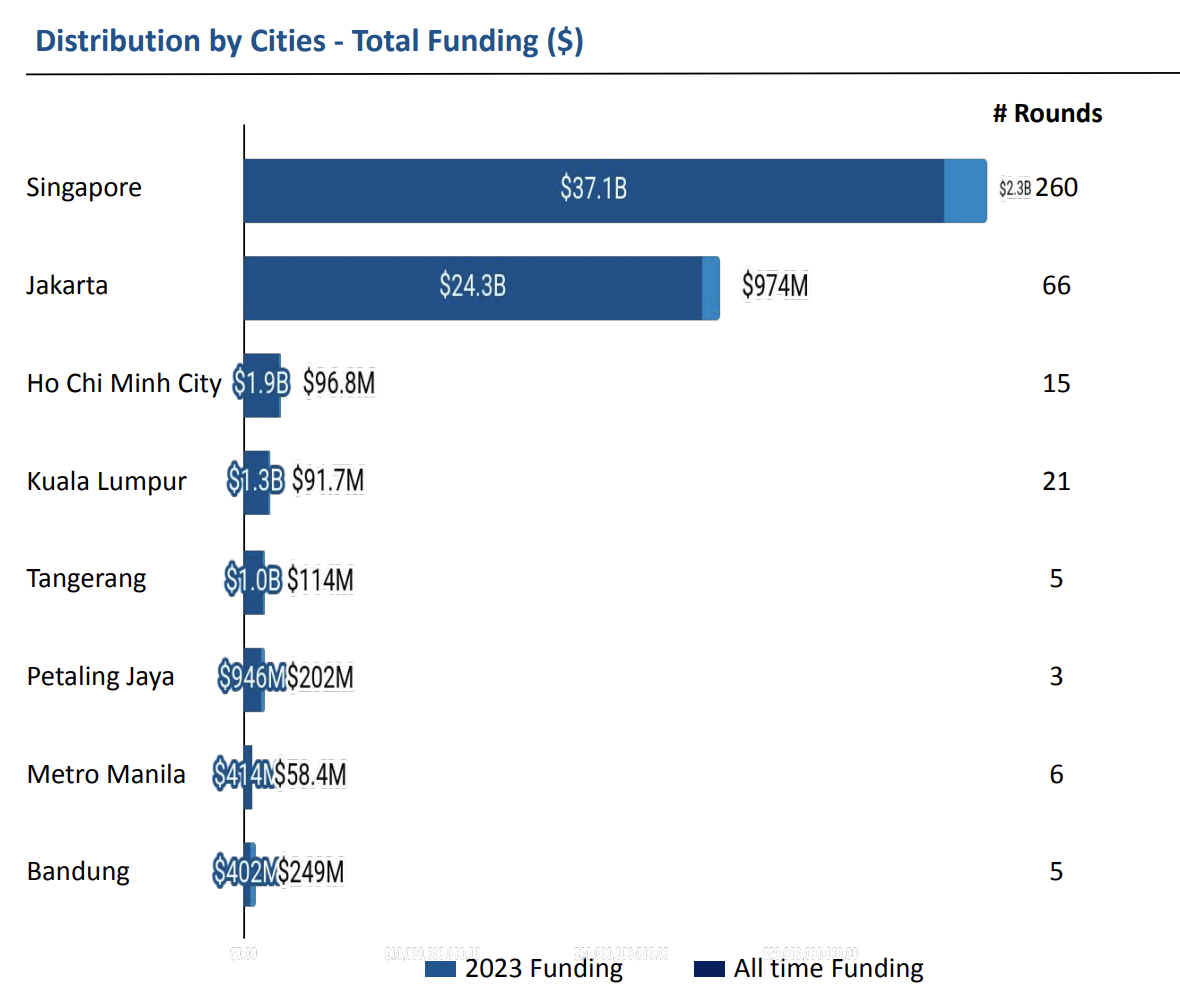

Singapore continued to dominate the tech landscape in 2023, accounting for 53% of all tech funding secured that year, data from Tracxn show. Jakarta followed suit, accounting for 33% of all tech funding in 2023.

Tech startup funding by cities in Southeast Asia, Source: Geo Annual Report, Southeast Asia Tech – 2023, Tracxn, Dec 2023

Featured image credit: edited from Freepik

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/85423/funding/southeast-asia-fintech-holds-strong-despite-tech-investment-pullback/