In Asia-Pacific (APAC), the nascent wealthtech sector is poised to witness strong growth, a rise which will be driven by technological advancements, the region’s increasing wealth as well as its large affluent segment which has so far remained largely untapped and underserved, a new report by global consultancy McKinsey claims.

The report, titled WealthTech in Asia-Pacific: The next frontier in financial innovation, discusses the rapid growth and transformation of the wealth management industry in the APAC region, stressing how this growth has been driven by technological advancements, changing customer behaviors and favorable demographics.

According to the report, wealthtech solutions, which utilize technology and digital platforms to increase efficiencies and facilitate activities across the wealth management value chain, are rapidly gaining momentum in APAC, promising a plethora of opportunities for wealth management firms, including improved accessibility, enhanced efficiency and greater services personalization.

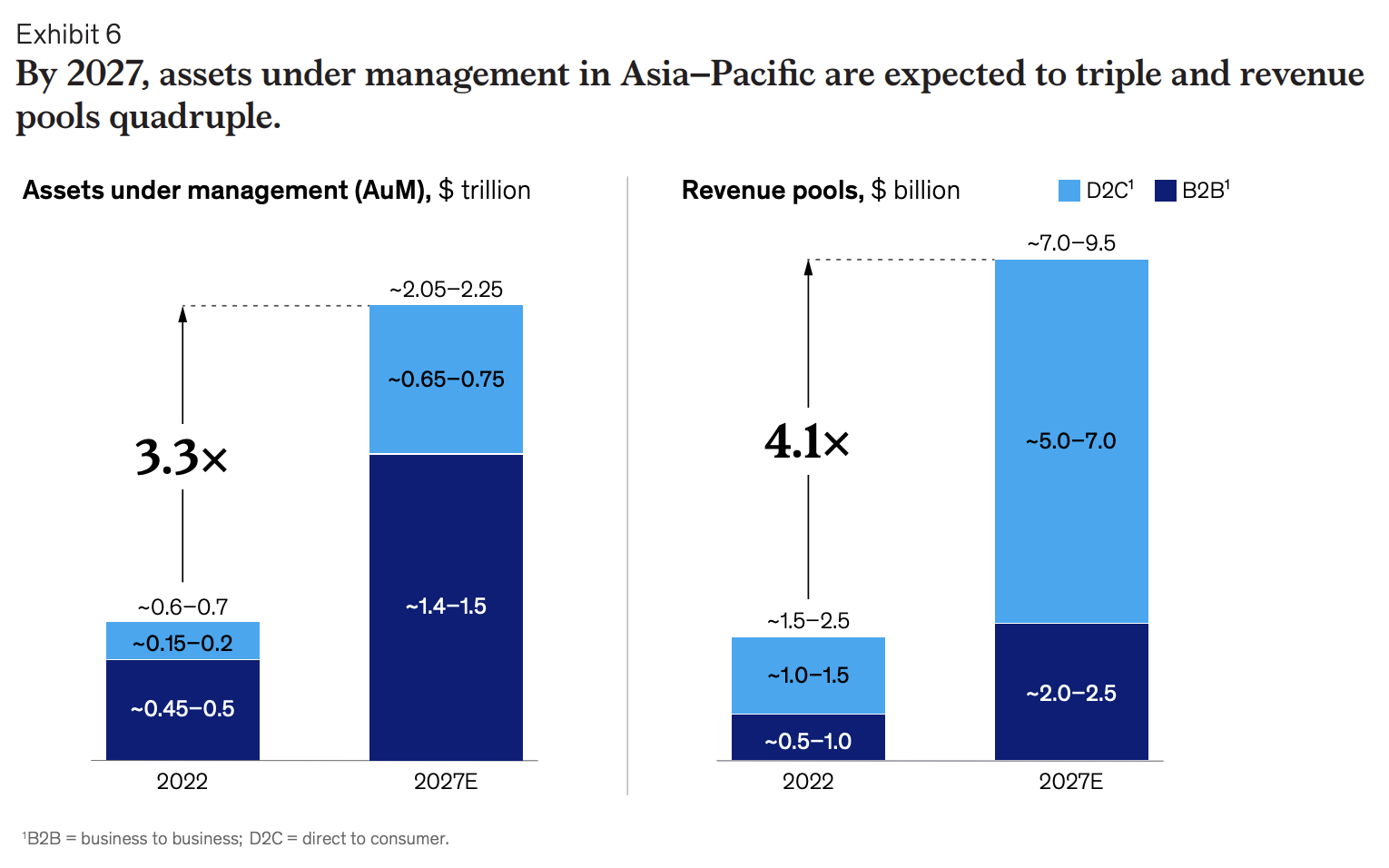

Although the sector remains nascent, managing about US$600-700 billion worth of assets at the end of 2022, wealthtech is on the brink of substantial expansion and is poised to transform the wealth management landscape.

By 2027, APAC’s wealthtech industry is expected to grow by approximately 25-30% per year and could triple or even quadruple its present assets under management (AUM) and revenues by then, McKinsey predicts. That would translate to the market reaching a US$2.05-2.25 trillion valuation by 2027, soaring from the US$600-700 billion value reported in 2022.

A breakdown of key wealthtech categories shows that direct-to-consumer (D2C) wealthtech solutions, which comprise multi-asset, digital platforms that offer publicly traded assets and private assets, together with either pure digital or hybrid advisory, will be recording the strongest growth. By 2027, the segment is projected to overtake business-to-business (B2B) wealthtech in terms of revenue pools, making up the lion’s share of the overall wealthtech market.

By then, D2C wealthtech revenues are set to surge to US$5-7 billion, representing a ~3-7x increase from 2022’s US$1-1.5 billion, McKinsey predicts. Assets under management (AUM) could reach US$650-750 billion, representing a ~3-5x increase from US$150-200 billion in 2022.

Meanwhile, business-to-business (B2B) wealthtech, which encompasses firms catering to financial institutions and advisors, is projected to grow at a more moderate pace, with revenue pools expected to reach US$2-2.5 billion in 2027, representing a ~2-5x increase from US$0.5-1 billion in 2022, McKinsey predicts. AUM are set to reach US$1.4-1.5 trillion by 2027, up ~2-3x times from 2022’s US$450-500 billion.

In 2022, B2B wealthtech had a market size of US$450-500 billion. By 2027, McKinsey estimates that the sector could grow by approximately 25% per year to US$1.4-1.5 trillion.

APAC wealthtech assets under management and revenue pools, Source: WealthTech in Asia-Pacific: The next frontier in financial innovation, McKinsey, Oct 2023

APAC’s wealth opportunity

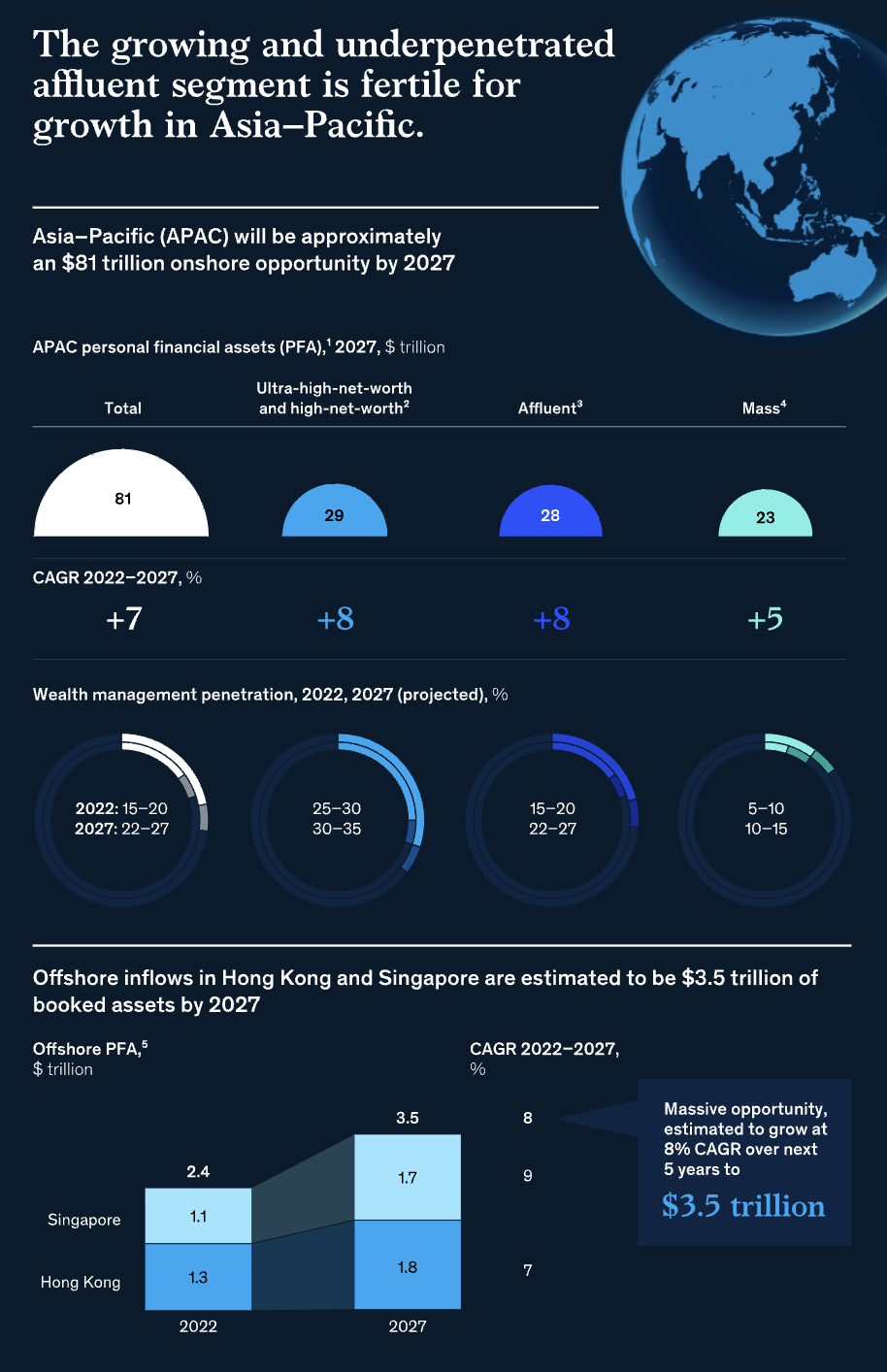

Wealth management remains a nascent industry in APAC, with just around 40-45% of personal financial assets (PFA) in cash and deposits. But with its growing economy and increasing wealth, the region is poised to become an important region in global wealth management.

By 2027, the onshore PFA are expected to reach around US$81 trillion, generating approximately US$1 trillion in revenue pools across the wealth continuum, McKinsey estimates.

By then, the affluent segment is poised to represent 34% of onshore PFA, growing at a compound annual growth rate (CAGR) of 8% from 2022 to 2027. This segment has notably remained untapped and underserved and has a comparatively low wealth management penetration of 15 to 20% as of today, the consultancy argues.

Asia-Pacific’s growing affluent segment, Source: WealthTech in Asia-Pacific: The next frontier in financial innovation, McKinsey, Oct 2023

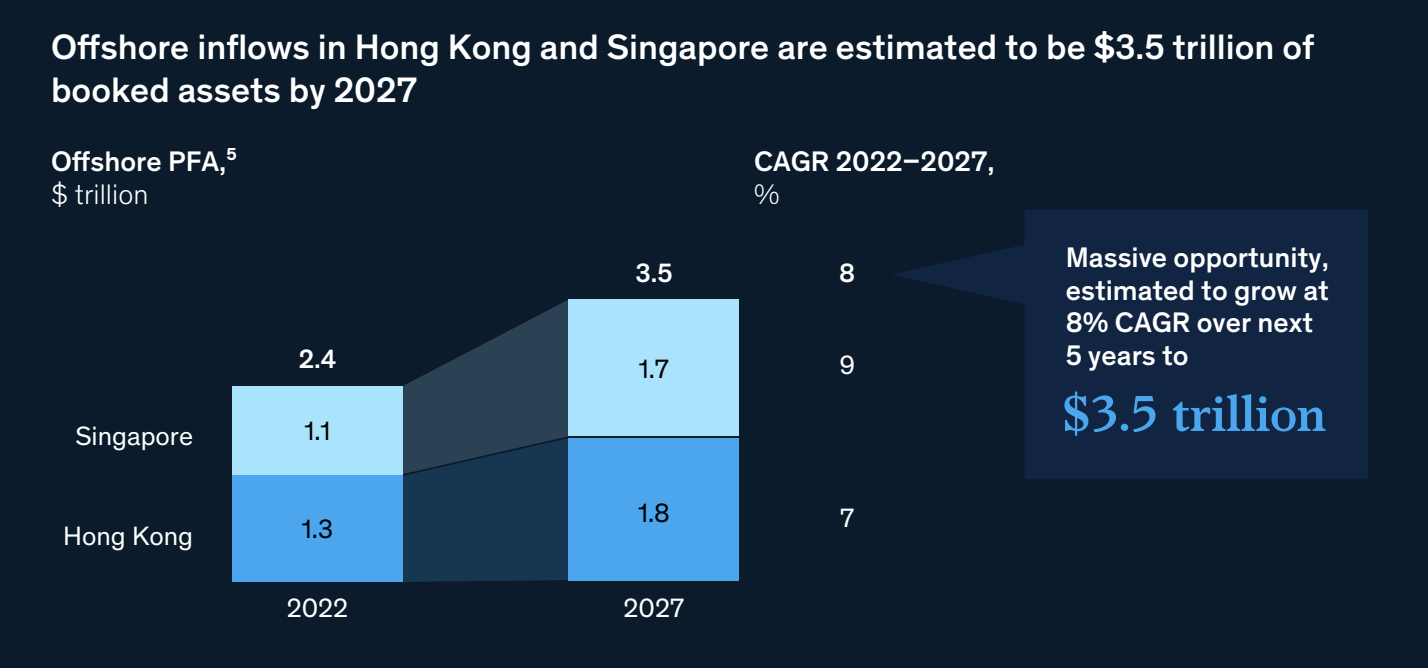

At the same time, “cross-border wealth management connectivity” is also increasing, with substantial flows to key Asian booking centers, particularly Hong Kong and Singapore, expected to reach around US$3.5 trillion in booked assets by 2027, growing at a compound CAGR of 8% per annum from 2022 to 2027.

Offshore inflows in Hong Kong and Singapore (US$ trillion), Source: WealthTech in Asia-Pacific: The next frontier in financial innovation, McKinsey, Oct 2023

Besides favorable economic and demographic factors, the digital wealth opportunity in APAC is also evidenced by a clear interest from consumers in these new tech-enabled products.

In McKinsey’s 2021 Personal Financial Services Survey, approximately 80% of affluent and mass-affluent respondents in Asia – defined as households with investable assets of US$100,000 to US$1 million – said they would or might consider receiving advisory services remotely through digital channels.

Local players are also witnessing strong growth. In Singapore, digital wealth manager StashAway surpassed US$1 billion in AUM in the span of 3.5 years, and has, since its inception in 2016, expanded to Malaysia, the Middle East and North Africa, Hong Kong, and Thailand. Endowus, another digital wealth platform from Singapore, crossed S$1 billion (US$740 million) in AUM in less than two years of full launch.

Featured image credit: Edited from freepik

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://fintechnews.sg/80671/wealthtech/wealthtech-in-apac-report-2027/