- A less dovish Fed with a surprise cut by SNB has triggered a bout of US dollar strength since last Thursday, 21 March.

- China’s central bank, PBoC responded with a lower-than-expected daily fixing on the onshore yuan (CNY) last Friday, 22 March which led the offshore yuan (CNH) to plunge by -0.8% against the US dollar to a two-month low.

- Further CNH weakness may trigger a currency war which in turn can trigger a potential negative feedback loop back into risk assets.

This is a follow-up analysis of our prior report, “Hang Seng Index Technical: The countertrend rebound phase may have ended” dated 5 March 2024. Click here for a recap.

In the past two weeks, China, and Hong Kong benchmark stock indices (CSI 300, Hang Seng Index, Hang Seng TECH Index & Hang Seng China Enterprises Index) have traded sideways after recording gains of between +16% to +24% from their respective early February lows to recent mid-March highs.

These recent bouts of positive performances have propelled China and Hong Kong to be the top-performing major stock markets in February and are supported by the absence of a strong US dollar environment that reduces the risk of capital outflows as China remains mired in a deflationary risk spiral as well as ongoing high tech trade war with the US since 2018.

Hence, the recent rallies and outperformance of the key China and Hong Kong benchmark stock indices have been indirectly supported by a stable Chinese yuan where the CNH (offshore yuan) has traded in a tight range of 0.7% against the US dollar between 5 February to 12 March.

SNB surprised rate cut may trigger a currency war

Last Thursday, 21 March, the Swiss National Bank (SNB) engineered a surprise on market participants by enacting a rate cut of 25 basis points (bps) to 1.5% on its key policy rate, its first cut in nine years, and ahead of the US Federal Reserve, Bank of England (BoE), and European Central Bank (ECB).

One of the push factors for enacting an earlier rate cut by SNB other than a clear deceleration in inflationary trend (annualized core inflation rate has remained below 2% since May 2023) is the persistent strength of the franc that could erode the competitiveness of Swiss goods and services which in turn put a dent on economic growth in Switzerland.

The EUR/CHF cross pair has accelerated its decline in the past three years where it tumbled by -17% to print a close of 0.9270 on 5 January 2024, a fresh all-time low on a closing level basis since the surprise EUR/CHF unpeg on 15 January 2015 (intraday low of 0.8600 with a daily close of 0.9753).

The CHF tumbled after the surprise SNB’s decision; it fell by -1% against the EUR to its weakest level since July 2023. Also, it dropped -1.2% against the US dollar to hit a fresh four-month low.

Interestingly, the offshore yuan (CNH) tumbled by -0.8% against the US dollar to print a two-month low last Friday, 22 March after the China central bank, PBoC set a weaker-than-expected daily fixing on the onshore yuan (CNY).

This latest set of FX policy moves by PBoC is likely to have signaled a willingness to sacrifice some form of capital outflows over maintaining exports’ competitiveness to drive economic growth, and to fill the gap in the absence of robust domestic demand.

If the US dollar continues to strengthen due to the Fed’s less dovish stance (in no hurry to cut rates), it may lead to a bout of engineered currency devaluations among major exporters such as South Korea and Singapore which is likely to put pressure on PBoC to weaken the CNH further to make up for a further potential loss of trade competitiveness.

Overall, a persistent US dollar strength trend may trigger “beggar-thy-neighbour” currency war-liked monetary policies among exporters.

A weaker CNH does not bode well for risk assets

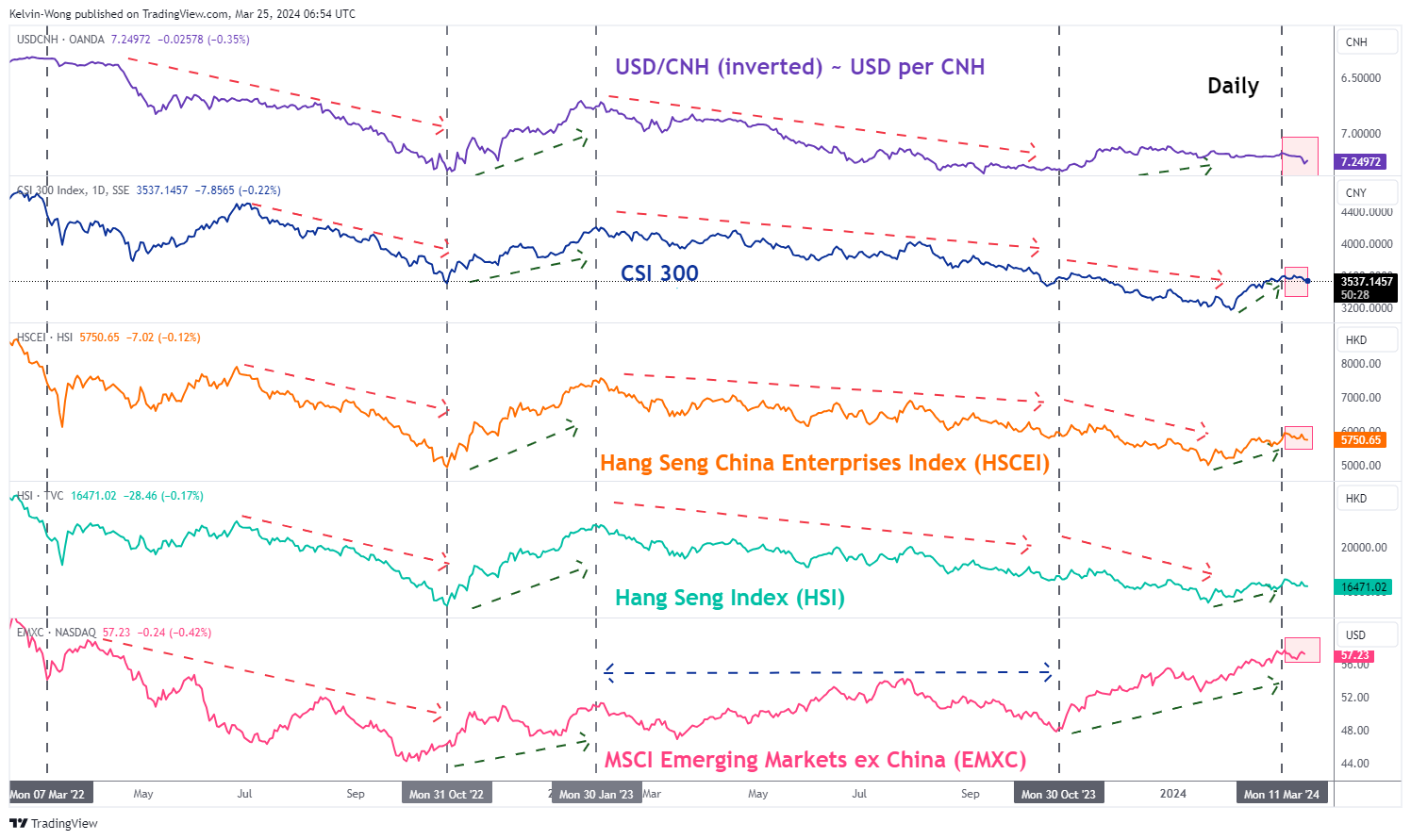

Fig 1: CNH/USD direct correlation with CSI 300, HSCEI & HSI as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

In the past two years, periods of significant weakness in the CNH (offshore yuan) against the US dollar have triggered a negative feedback loop back into the China and Hong Kong stock markets but to a lesser extent in emerging stock markets excluding China (see Fig 1).

Therefore, the recent softness seen in the CNH may trigger another round of potential multi-week bearish movements in the CSI 300, Hang Seng China Enterprises Index, and Hang Seng Index.

Bearish momentum has resurfaced in the Hang Seng Index

Fig 2: Hong Kong 33 Index major trend as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

Fig 3: Hong Kong 33 Index short-term trend as of 25 Mar 2024 (Source: TradingView, click to enlarge chart)

The price actions of the Hong Kong 33 Index (a proxy on the Hang Seng Index futures) have staged a bearish breakdown below its former ascending channel support in place since the 22 January 2024 low and its 20-day moving average on last Friday, 22 March.

In addition, the daily RSI momentum has also broken below its key parallel ascending support and just breached below the 50 level which indicates a potential revival of medium-term bearish momentum.

In the lens of technical analysis, this latest set of bearish elements suggests the recent rally of +16% from the 22 January 2024 low of 14,777 has taken the form of a “bearish flag” configuration, aka countertrend rebound motion within its major and long-term secular bearish trend phases (see Fig 2).

Last Friday’s bearish breakdown seen in the “bearish flag” and its daily RSI suggested a likelihood that the bearish impulsive down move sequence has resumed.

If the 16,960 key short-term pivotal resistance is not surpassed to the upside, the Index may see a further potential decline to expose the next intermediate supports at 16,135 (also the 50-day moving average), and 15,730 (see Fig 3).

However, a clearance above 16,960 negates the bearish tone to see a retest on the 17,230 minor swing high area of 13 March 2024, and above it sees the medium-term pivotal resistance coming in at 17,570/600.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Passionate about connecting the dots in the financial markets and sharing perspectives around trading and investment, Kelvin Wong is an expert in using a unique combination of fundamental and technical analyses, specializing in Elliott Wave and fund flow positioning, to pinpoint key reversal levels in the financial markets.

In addition, over the last ten years, Kelvin has conducted numerous market outlook and trading-related seminars, as well as technical analysis training courses, for thousands of retail traders.

Latest posts by Kelvin Wong (see all)

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.marketpulse.com/indices/hang-seng-index-potential-currency-war-may-kick-start-another-bearish-leg/kwong