Charles Edwards, the founder of Capriole Investments, has sparked significant interest and debate within the cryptocurrency community. He heralded Ethena (ENA) as “the Luna of this cycle,” but with a crucial difference: its economic fundamentals are deemed sustainable.

Edwards elaborated, “It’s 100% collateralized and the yield is variable based on market forces. Two things Luna wasn’t.” He also noted that at its zenith, Luna’s valuation exceeded ENA’s current market cap by more than twenty-fold, yet he cautioned, “ENA is not risk-free, custody and execution risk exist.”

Ethena is the Luna of this cycle, except the underlying economics are actually sustainable. It’s 100% collateralized and the yield is variable based on market forces. Two things Luna wasn’t. At it’s peak LUNA was over 20X bigger than what ENA is now. ENA is not risk free, custody…

- Ο Charles Edwards (@caprioleio) Απρίλιος 10, 2024

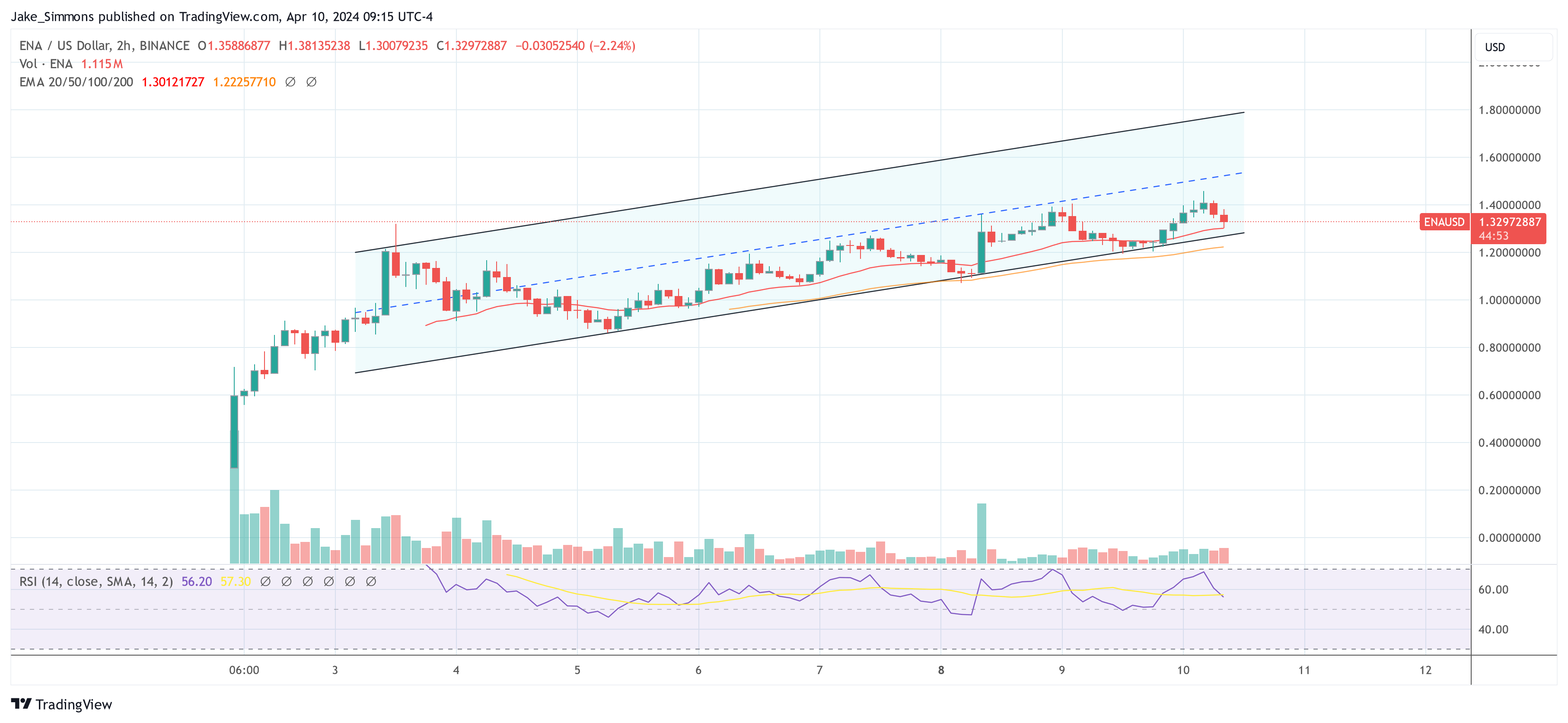

Since its launch on April 2, ENA has seen a μετεωρική άνοδο from under $0.30 to a high of $1.45. This rally is largely attributed to Ethena Labs’ strategic enhancement of its rewards program, now in its “Season 2,” which offers a 50% reward boost for users locking their ENA tokens for at least seven days. This move aims to bolster user engagement and loyalty, fostering a sustainable ecosystem for the Ethena platform.

A remarkable aspect of this ecosystem is the rapid growth of its stablecoin, USDe, which has outstripped the supply growth of established counterparts such as USDT, USDC, and DAI, reaching a $2 billion supply in just over 100 days.

Το USDe είναι το ταχύτερα αναπτυσσόμενο περιουσιακό στοιχείο σε USD στην ιστορία της κρυπτογράφησης pic.twitter.com/xgiRJjf96t

— G | Αιθένα (@leptokurtic_) Απρίλιος 8, 2024

However, the project’s high yields which are generated by harnessing the derivative markets and staked Ethereum have stirred skepticism among industry experts. Fantom founder Andre Cronje, among others, has raised concerns about the sustainability of these yields, which are the highest in the entire crypto industry.

Risks Involved With Ethena

Noteworthy, ENA is often compared to Terra Luna (LUNA), but the differences could not be much bigger, as Edwards also noted. While ENA is not risk free, a demise like the one of LUNA is highly unlikely. Despite that, investors need to be aware of other risks involved with ENA.

Diving deeper into the discussion of risks, CL (@CL207) from eGirl Capital offers an intriguing perspective on the behavior of derivatives traders. She αποσαφηνίζει, “It appears Ethena is making many people who don’t trade derivatives have a really hard time wrapping their heads around the fact that derivatives traders are so genuinely retarded that we’re willing to pay like 50%+ APR to enter a position.”

Notably, last cycle crypto traders were bidding futures so high that Bitcoin quarterlies earned “a locked-in >50% apr. She added, “just 50 days into 2021, we collectively paid 2,400,000,000$ in funding rates by the end of 2021, the market has paid as much as a decently sized country’s GDP.”

Monetsupply.eth (@MonetSupply) from Block Analitica provides a granular analysis of the risks Andre Cronje highlighted. Through his εξέταση, several key areas of concern are outlined:

- Oracle Risk: The potential impact on exchange positions due to Ethena providing inaccurate quotes on minting or redeeming operations. However, MonetSupply notes, “there’s rate limits on this tho so max loss is constrained and counterparties are all whitelisted (can’t just run away with the money).”

- Κίνδυνος εκκαθάρισης: Deemed not a significant factor as the portfolio is leveraged less than 1x, suggesting a conservative approach to borrowing and leverage.

- Διασπορά κινδύνου: The possibility of increased basis leading to higher funding revenue, which should theoretically attract inflows. Conversely, a negative basis might cause outflows, but Ethena could benefit from closing hedged positions profitably.

- Collateral Ratio Risk: Even though liquid staking tokens (LSTs) are given less than 100% weight on centralized exchanges (CEX), the overall low leverage mitigates this risk. The proportion of LST in spot collateral is relatively minor.

- Custody Risk: Highlighted as one of the more significant concerns, given the reliance on custodians with a good track record and the distribution of assets across multiple entities.

- Exchange Solvency Risk: This risk could lead to the loss of unsettled profit and loss (PnL) and some trading costs to rehedge on other exchanges. However, MonetSupply adds, “the Binance/ceffu nexus might change this assessment though, are they actually independent?”

- Ethena Entity Risk: The internal risk related to Ethena’s keys or authentication tokens being compromised, or a team member acting maliciously.

MonetSupply concludes that despite these risks, the framework of overcollateralization on platforms like Morpho, the Maker surplus buffer, and the MKR backstop, supported by a substantial Proof of Liquidity (POL), serves as a robust mitigating factor.

At press time, ENA traded at $1.329.

Featured image from Bitget, chart from TradingView.com

Αποποίηση ευθύνης: Το άρθρο παρέχεται μόνο για εκπαιδευτικούς σκοπούς. Δεν αντιπροσωπεύει τις απόψεις του NewsBTC σχετικά με το αν θα αγοράσει, να πουλήσει ή να κρατήσει οποιαδήποτε επένδυση και φυσικά η επένδυση ενέχει κινδύνους. Σας συμβουλεύουμε να διεξάγετε τη δική σας έρευνα πριν λάβετε οποιαδήποτε επενδυτική απόφαση. Χρησιμοποιήστε τις πληροφορίες που παρέχονται σε αυτόν τον ιστότοπο αποκλειστικά με δική σας ευθύνη.

- SEO Powered Content & PR Distribution. Ενισχύστε σήμερα.

- PlatoData.Network Vertical Generative Ai. Ενδυναμώστε τον εαυτό σας. Πρόσβαση εδώ.

- PlatoAiStream. Web3 Intelligence. Ενισχύθηκε η γνώση. Πρόσβαση εδώ.

- PlatoESG. Ανθρακας, Cleantech, Ενέργεια, Περιβάλλον, Ηλιακός, Διαχείριση των αποβλήτων. Πρόσβαση εδώ.

- PlatoHealth. Ευφυΐα βιοτεχνολογίας και κλινικών δοκιμών. Πρόσβαση εδώ.

- πηγή: https://www.newsbtc.com/news/ethena-ena-luna-of-this-cycle/