- ECB keeps rates on hold as inflation and growth cool

- US Core PCE cools more-than-expected

- US continuing claims rise to the highest levels since May

The US dollar was slightly firmer after a dovish hold by the ECB and after a handful of US economic readings boosted soft landing hopes as the labor market softened, quarterly Core PCE cooled more than expected, and economic growth surged last quarter. Today’s round of earnings also highlighted a robust consumer last quarter but that outlook will sour as sticky inflation will likely persist. Mastercard, SouthWest, and Royal Caribbean provided good reasons to be cautious with the outlook given weakening demand trends due to rising costs and the rising risk of an economic downturn.

Risk appetite isn’t ready to return until bond yields are sharply lower, which probably won’t happen until we see inflation a lot closer to the Fed’s target.

ECB – A dovish pause

The ECB’s extraordinary streak of interest-rate increases has ended as policymakers agreed to keeping rates on hold. As expected, all key rates were kept steady; main refinancing rate at 4.50%, deposit facility rate at 4.00% and marginal lending facility at 4.75%. Inflation clearly remains a concern as they highlight that “Inflation is still expected to stay too high for too long, and domestic price pressures remain strong.” The statement didn’t have any changes to PEPP, noting that they plan to “reinvest the principal payments from maturing securities purchased under the programme until at least the end of 2024.”

It is clear that inflation will continue to drop as the economy will remain weak for the rest of the year. After ten rate hikes, the ECB is likely done raising rates, but they won’t say they are done hiking. It will take time for them to get inflation to 2%, but it should happen next year as policy is restrictive enough.

US Data – as good as it gets

The US economy peaked in the third quarter. Robust spending helped real growth surge from 2.1% to 4.9% in the third quarter, above the consensus estimate of 4.5%. Personal consumption impressed as expected, rising 4.0% last quarter. The good news is that the economy was mostly unfazed with tightening of financial conditions. The bad news is that capital expenditures plunged 3.8%, which was down from 7.7% gain seen in Q2.

The September durable goods reading was rather impressive and provides some optimism for the manufacturing sector. A robust recovery for manufacturers however remains unlikely as the economy appears poised to soften given the deteriorating global growth outlook.

The weekly jobless claims report provided hints that the labor market is starting to weaken. Initial unemployment insurance claims rose by 210,000, above the 207,000 estimate and 200,000 upwardly revised prior reading. Continuing claims increased by 1.79 million, well above the 1.74 million estimate, reaching highest levels since May.

The third quarter Core PCE showed pricing pressures cooled quickly from 3.7% to 2.4%. Wall Street is going to expect tomorrow’s PCE core deflator might come in softer than expected. The disinflation process remains intact and that should pour some cold water on the surge with Treasury yields.

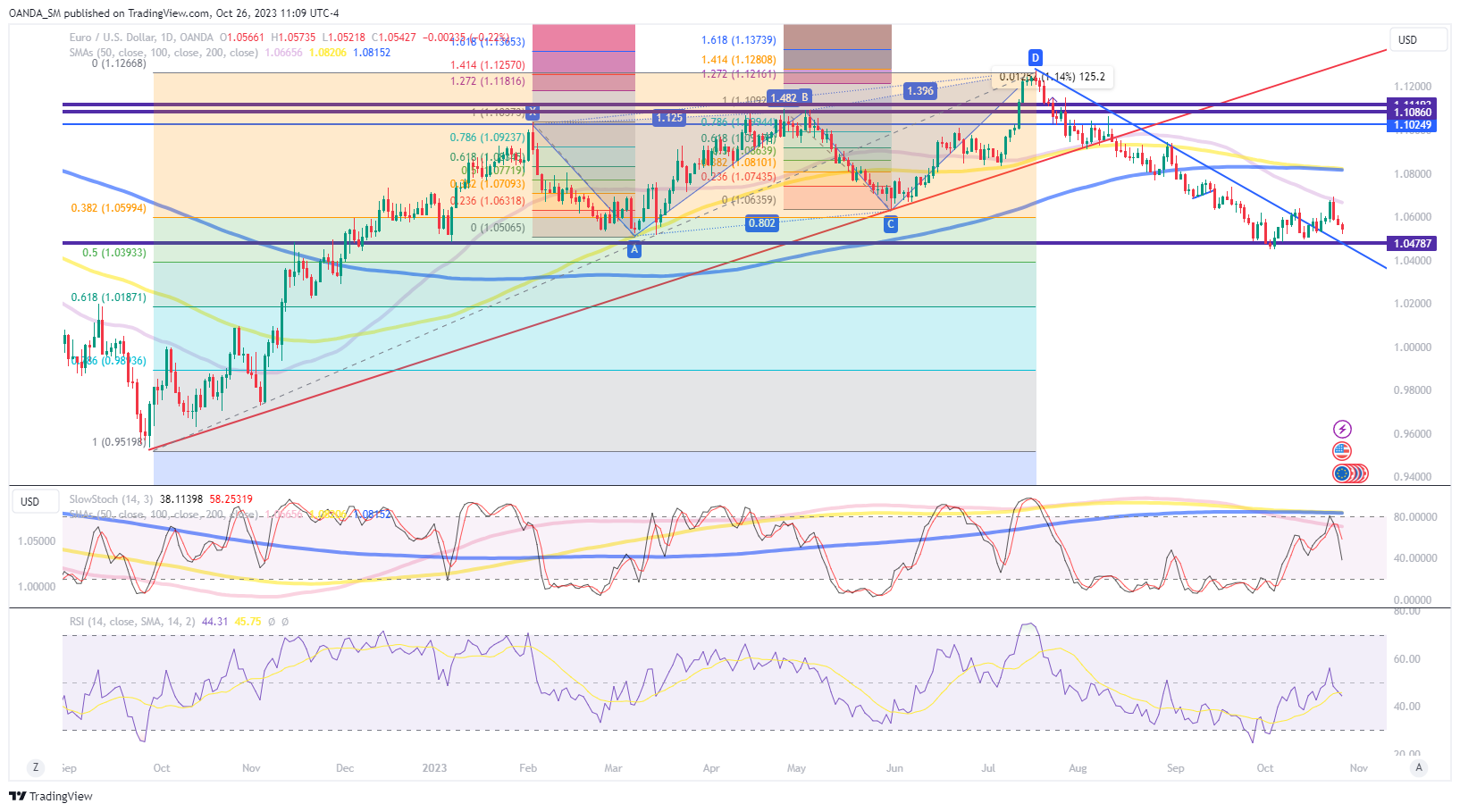

EUR/USD Daily Chart:

The euro rebounded stalled after price action failed to close above the 50-day SMA. The bearish trend appears intact as the US growth outperformance to Europe seems like it will last a while longer.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at [email protected]. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Ed Moya

- SEO Powered Content & PR Distribution. Get Amplified Today.

- PlatoData.Network Vertical Generative Ai. Empower Yourself. Access Here.

- PlatoAiStream. Web3 Intelligence. Knowledge Amplified. Access Here.

- PlatoESG. Carbon, CleanTech, Energy, Environment, Solar, Waste Management. Access Here.

- PlatoHealth. Biotech and Clinical Trials Intelligence. Access Here.

- Source: https://www.marketpulse.com/newsfeed/ecb-react-euro-softer-post-dovish-hold-and-robust-us-data/emoya