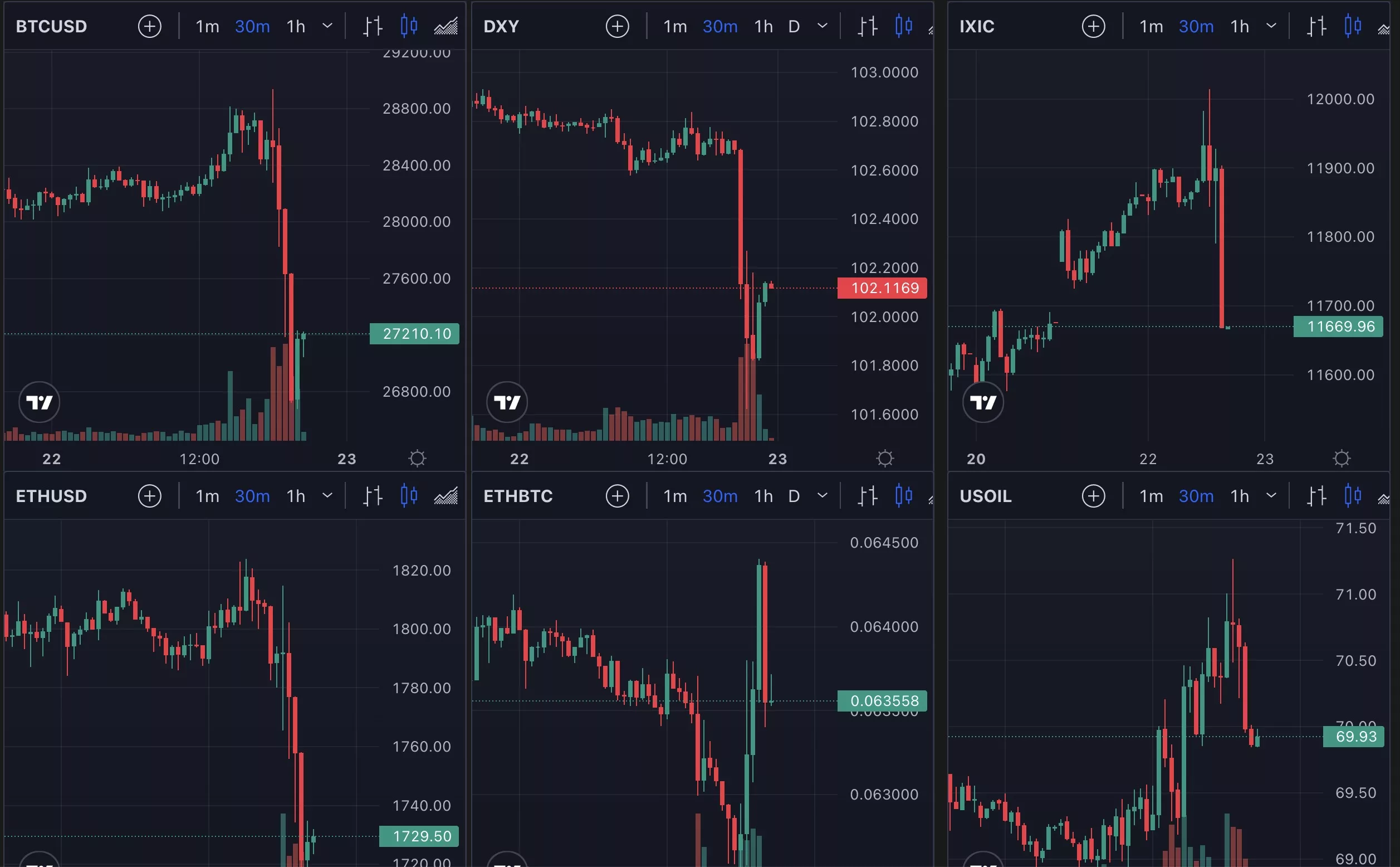

Bitcoin briefly dived below $27,000 after first trying to reach $29,000 earlier today amid yet another hike Wednesday.

What was a 50/50 split market on whether they will increase interest rates, became 80% certain over the past 24 hours as the decision was leaked.

There was no reaction to the leak however with stocks opening slightly green while bitcoin suggested it might take $30,000.

Yet an hour or so before Powell’s speech, bitcoin breached below $28,000, and then went on to fall to $27,000.

Nasdaq also saw some volatility as it spiked to just about touch 12,000 before falling to 11,700, down 1.6%.

This volatility may be in part because Powell has brought in some vagueness. The guidance has now changed from expect more hikes to expect “additional policy firming.”

What does that mean? Well, to keep something firm means to stop, with our initial interpretation of it being that it is another way of saying pause, but others are interpreting it as there will be only one more hike and then pause.

The committee however expects the fed rate to be at 5.1% at the end of the year if the economy evolves as projected. So another hike, if there is one, might be by just 10 basis points.

Not that 10 or 20 would make much of a difference at this point as the market find itself for the first time at the end of rate hikes, certainly looking 6 months ahead.

So why the price action today? Well, this ending of hikes does not come in normal circumstances. Fed expects a credit crunch, with some estimating the tightening of the bank lending might itself amount to a hike of 1.5%.

Powell did not explain, and was not asked, about just how severe he expects this credit crunch to be, but stated that it is a new development so they are keeping a close eye and will observe in the weeks to come the extent of this credit crunch.

Not that a tightening in bank lending was any new information considering the events of the past two weeks, but it is not clear whether the stock market has digested that aspect to a sufficient extent as they have been far too busy with immediate considerations of bank collapses.

In addition considering that Powell himself said this crunch amounts to a rate hike or it is comparable, him nonetheless hiking just for posturing – and that’s what he basically said though in more words in regards to showing confidence they will tackle inflation and yadayada – may have plenty wondering whethere these guys are just playing mind games instead of engaging in the very difficult task of trying to objectively ascertain what the best rate is for the economy.

A hike therefore by the central bank after commercial banks ‘hiked’ by 1.5%, makes this a super tightning.

But, Fed is pausing, yet no relief is to be expected this year in regards to any rate cuts. Next year they will cut, however the economy for an entire year will stay at what they themself have admitted is above neutral rates, even while banks collapse.

The potential for a recipe for disaster is obvious to all, but of course no one knows whether there will be any such thing, and it may well be the market looks forward to 8 or 9 months in coming down from the rollercoaster of hikes after up and up through it.

What the judgment will be therefore remains to be seen as market signals have been very unreliable on the day of the speech itself, and so far in fact markets have tended to move in the opposite direction of the moves on speech day.

That would mean if that countertrend continues, markets may move up in the days and weeks to come, but of course the past doesn’t predict the future.

All depends on just to what extent we will see a credit crunch, with the confirmation of one by Fed’s chair himself being the first since 2008.

Fed’s chair was also asked about the minutes of the last meeting back in February mentioning the potential for a run on the banks. Was any indication of it by the San Francisco Fed, the chair was asked. “Will get back to you on that” was the answer.

The crunch on – well these are not small banks considering the GDP of Greece is $214 billion, about as much as was in deposits at SVB – may now have secondary effects and if there’s a credit crunch, that might also have its effects.

The outlook therefore has changed and in many ways to the very downside on the economy, but in the tech, crypto, and stocks sector we have had a fairly deep recession for more than a year now.

The question therefore is whether such potentially deep recession in the economy will be mirrored in asset prices, or whether assets will look ahead to the recovery with countermoves.

The question is also whether the recession will be deep, but regardless we have entered uncertain territory as sky high rates unseen since house prices were $20,000 are now combined with a credit crunch and a continued tightening by the central bank while governments do not in any way intervene to prevent a recession.

This is a combination of newness that no one under 30 or 40 has ever seen before, and therefore for the real economy we have been expecting for two months now a tougher time as GDP growth year on year has been on a significant downtrend in US.

But for assets, the question is just how much they will look forward to the cuts in nine months or so and to the recovery, and just how much instead they might respond to more immediate new developments, like an expected credit crunch.

That credit crunch being a hypothesis or expectation rather than reality adds more complexity to this analysis, but where crypto is concerned, it all sounds like 2023 might develop like the usual after bear year, that being some movement up, but keeping more for next year.

What stocks will do is less known, especially as they depend on the quarterly earnings season which begins now in two weeks.

- SEO Powered Content & PR Distribution. Get Amplified Today.

- Platoblockchain. Web3 Metaverse Intelligence. Knowledge Amplified. Access Here.

- Source: https://www.trustnodes.com/2023/03/22/bitcoin-and-stocks-dip-on-fed-hikes-but-is-it-a-fakeout